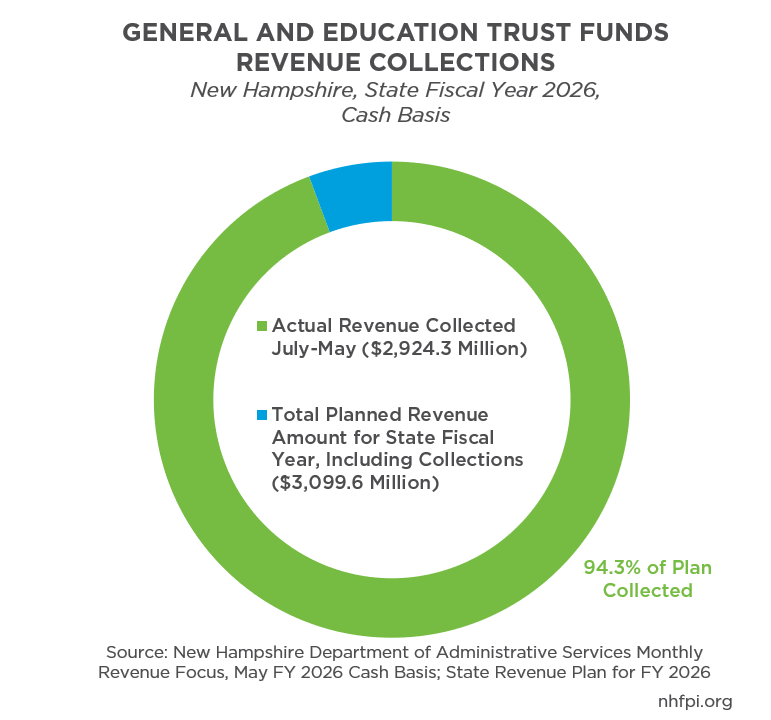

State revenue collections were above targeted amounts in May, adding to the State’s revenue surplus despite lower than planned revenues from the two primary business taxes, new video lottery machines, and liquor sales. May is not a critical month for State revenues, and the total amount of General and Education Trust Funds revenue collected was $143.5 million. This total increased the State’s revenue surplus for these two funds by $2.4 million, pushing the year-to-date total to $156.7 million, or 5.7% above the target amount for the end of May in the State Revenue Plan. The shortfalls in some sources were offset by higher-than expected revenue resulting from the ongoing tobacco settlement payments to the State, as well as later-than-expected securities revenue and interest earned on State cash holdings.

For State Fiscal Year (SFY) 2026 thus far, the leading contributors to the State’s cash surplus have been the Tax Amnesty Program, Insurance Premium Tax revenues, interest on State cash holdings, and revenues from the Lottery and Gaming Commission excluding Video Lottery Terminals. May’s receipts reflect the three biggest detractors from the State’s actual revenues relative to planned amounts for the year, with the combined Business Profits and Enterprise Taxes, revenues from the Liquor Commission, and Video Lottery Terminals falling furthest below target amounts for the year thus far.

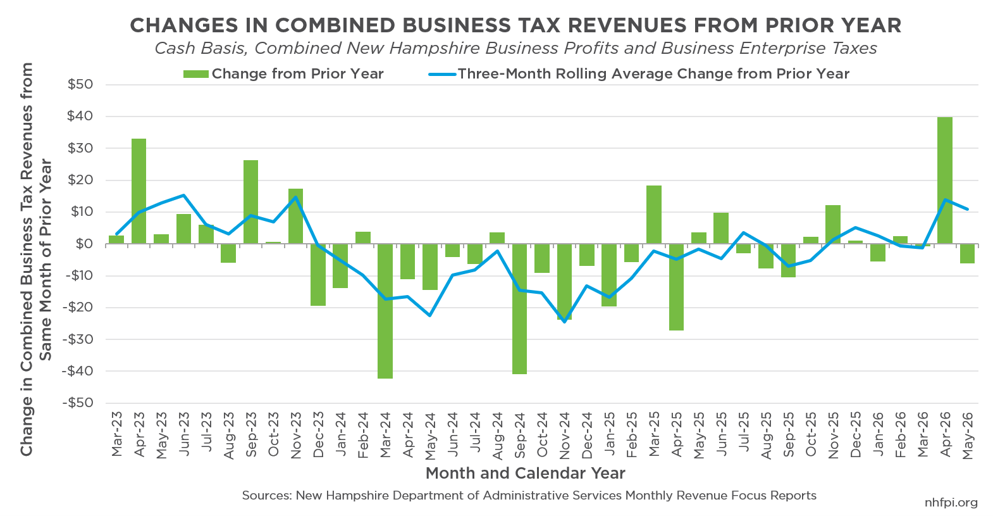

Business Tax Revenues Slip After Strong April Returns

Combined receipts from the State’s two primary business tax revenue sources were $6.2 million (19.0%) lower than planned amounts in May and were $5.9 million (18.3%) below receipts from May SFY 2025, unadjusted for inflation. The State reported an increase in business tax refunds relative to last May as contributing to this shortfall.

For the fiscal year ending on June 30 thus far, business tax revenues were $24.3 million (2.6%) above last year’s receipts through May, unadjusted for inflation, but fell short of the planned amount by $12.6 million (1.3%).

The slump in business tax receipts in May, which is not a key month for these revenues, follows strong collections from April, which included both returns and extensions from the prior year and the first quarterly estimate payments of the new tax year for most businesses. However, those strong April receipts were primarily due to tax payments based on last year’s activity and were not the result of elevated activity from the first quarter of the new tax year. Lackluster business tax performance in May could be reflecting some of the ongoing challenges with the current economic environment relative to last year’s tax activity.

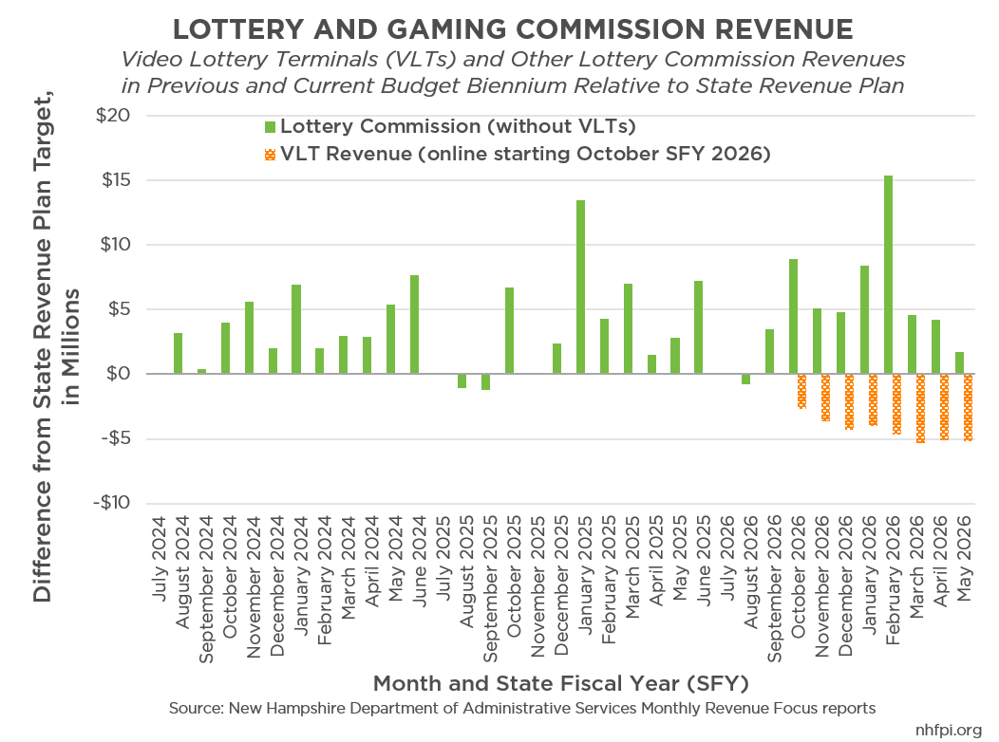

Gambling on Video Lottery Terminals

The State established Video Lottery Terminals (VLTs) as a new revenue source for SFY 2026. VLTs are devices that accept and dispense money, vouchers, or other credits to players who participate in games of chance at machines with spinning reels or video displays that are not connected to the internet. The State collects 31% of VLT revenue as a tax on the activity, with revenues going to support the Governor’s Commission on Addiction, Treatment, and Prevention; charitable gaming contributions to charities in New Hampshire; Lottery Commission operations; the Education Trust Fund; and the General Fund.

Projected SFY 2026 VLT revenue for the combined General and Education Trust Funds portion is $60.1 million, but actual VLT revenue has only been $15.9 million in the first eleven months of SFY 2026. In May, VLT revenue was $5.2 million (55.9%) below the planned $9.3 million for the month, constituting the largest shortfall of any single source outside of the business taxes relative to May’s targets.

For SFY 2026 thus far in total, profits from the other operations of the Lottery and Gaming Commission have offset the VLT revenue shortfalls. Overall Lottery and Gaming Commission revenues are $55.8 million (34.7%) ahead of planned amounts for SFY 2026 through May, more than counterbalancing the $34.9 million (68.7%) shortfall in VLT revenue compared to expectations.

However, the VLT shortfall relative to planned amounts has been larger than other profits from lottery operations during each of the last three months. Lottery revenues can change quickly, and more VLT sites will likely come online in future months, but VLT revenue may not be as significant during this State Budget biennium as policymakers projected.

One Month Left in the Year

The revenue upsides for May do not provide any strong indication of future revenue trends. Interest earned on State cash holdings continues to be higher than expected, but is still $29.6 million (28.8%) lower than last year and is likely to be a declining revenue source as State cash holdings have been diminished in part due to expenditures of one-time federal funds held by the State. Funding transferred as part of the Master Settlement Agreement between states and four large tobacco companies came in slightly higher and later than expected. Securities revenue payments to the State were also paid later and are about 0.9% below planned amounts, suggesting this revenue source is not growing, but that May’s receipts above targets were a result of timing rather than growth.

June, which is the last month of SFY 2026, could offer some stronger indications of long-term trends. Revenues will include quarterly estimate payments from many businesses, as well as some Meals and Rentals Tax revenues from the May activity that will be included in June receipts.

The State will likely end SFY 2026 with more combined General and Education Trust Funds revenue than originally anticipated, largely due to the Tax Amnesty Program generating $98.8 million more for these funds than policymakers projected. The State Revenue Plan anticipates that June SFY 2026 will generate $332.0 million in revenue, and receipts would have to fall below $175.3 million to leave the State in a revenue deficit based on actual revenues through the end of May.

However, the revenue surplus reflects the projections from when the State Budget was crafted, and if policymakers need to spend more money than planned, the revenue surplus could still miss covering all expenses. For example, if the State needs to pay more in Youth Development Center claims, additional General Fund resources may be needed beyond the amounts envisioned in the State Budget.

Even with those potential additional costs, these revenues are, in aggregate, more favorable than were anticipated earlier in the year by State forecasters. Another year of revenue that exceeds expectations would add to the resources available to craft the next State Budget and fund services for the SFYs 2028-2029 period.