New Hampshire’s Tax Amnesty Program generated much more one-time State revenue than predicted by legislators, and nearly all the collections were due to previously unpaid business taxes.

Amnesty Program Gives Breaks to Late Taxpayers

The Tax Amnesty Program allowed people and businesses with unpaid taxes to pay past-due amounts without the usual nonpayment penalties that the State typically charges, and permitted 50% lower interest costs due to the later payments than typically would be charged. The Program, which was established by the State Budget and ran from December 1 to February 15, was projected to generate $5.0 million for the combined General and Education Trust Funds in the Legislature’s forecasting.

Instead, this cost-saving measure for people and businesses with overdue and unpaid taxes brought in $103.8 million during its short existence, or nearly 21 times the amount of revenue the Legislature forecast it would generate. While not all tax revenue sources flow to the State’s General and Education Trust Funds, all revenue paid through the Tax Amnesty Program flowed to these two funds.

While the identities of individual filers are protected by taxpayer privacy laws, the New Hampshire Department of Revenue Administration has provided additional information about the people and businesses taking advantage of the Program during its 2.5-month lifespan. The Program brought in more revenue than the most recent previous similar program, particularly from business taxpayers, and also raised a significant amount of money from the closure of ongoing audits and collections cases.

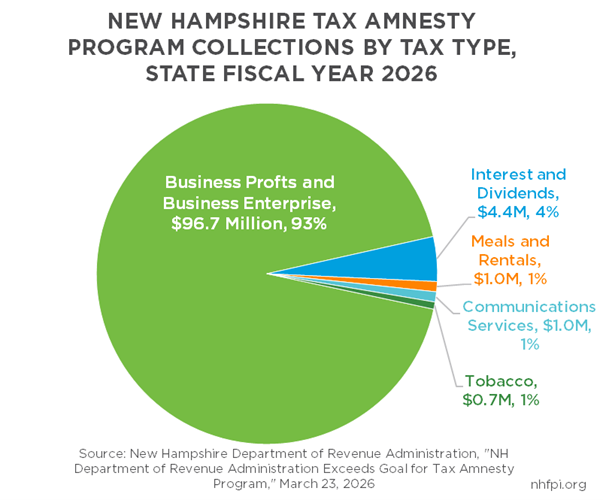

More Revenue Than Last Amnesty Program

The State Fiscal Year (SFY) 2026 Tax Amnesty Program brought in much more revenue than the most recent Tax Amnesty Program. The SFY 2016 iteration generated $19.0 million, with 81.0% of that total generated by the Business Profits Tax and the Business Enterprise Tax combined. About 8.1% ($1.5 million) of the SFY 2016 Program’s revenue came through the Meals and Rentals Tax, while 7.3% ($1.4 million) were dollars that had been owed to the State through the Interest and Dividends Tax.

Of the $103.8 million generated in the SFY 2026 Tax Amnesty Program, 93.2% ($96.7 million) were collected through the combined business taxes, potentially reflecting both the growing importance of the business taxes in State revenues since 2016 and the changes in the structures of the businesses taxes that could have generated unanticipated tax liability for businesses. Another 4.2% ($4.4 million) was collected through the Interest and Dividends Tax, and the State reported the remainder were in Meals and Rentals Tax ($1.0 million), Communications Services Tax ($1.0 million), and Tobacco Tax ($0.7 million) collections. If other taxes contributed smaller amounts, they were not reported in detail, potentially to protect taxpayer privacy.

The total amount of tax amnesty collections in SFY 2026 was about 447.6% higher than the amount of SFY 2016’s collections, even though total General and Education Trust Funds revenue rose only 36.8% between SFYs 2015 and 2025, the years before each amnesty program.

Before SFY 2016, the State Legislature also used the State Budget to authorize tax amnesty programs in 2001 for all taxes collected by the Department of Revenue Administration, and in 2005 solely for the Real Estate Transfer Tax.

Audits and New Taxpayers

According to the Department, the revenue coming into the Tax Amnesty Program resulted from routine payments and assessments, closing out audits and collections cases, and the identification of new filers who were not previously paying taxes.

Of these groups, the audits generated the most revenue. About $79.5 million, collected from 692 returns, were collected related to audit processes. About 94.6% of these revenues came through business taxes. The average amount collected for each filing through the audit closeouts in the Tax Amnesty Program was about $115,000. Data are not available by filer type, but larger business taxpayers likely contributed much higher amounts than that average, as the 1.2% from Communication Services Tax audits and 1.5% from Meals and Rentals Tax and Tobacco Tax audits combined were likely comparatively small amounts of revenue.

Collections closeouts generated $11.0 million in Tax Amnesty Program revenue from 1,780 returns, or about $6,200 per filing. About 87.3% of revenues were through business tax filings in this category.

The Tax Amnesty Program also brought new filers to the awareness of the Department of Revenue Administration and into compliance with State tax law. The comparatively small amount of revenue, $3.4 million, reflected 850 returns, about 91.7% of which were through business taxes.

Unknowns and Considerations

The Tax Amnesty Program successfully boosted State revenue, but the public does not have clarity as to the amount of money that would have been generated if taxpayers had paid the overdue taxes and interest costs without the program. The program was given a budget of $50,000 to implement, of which $40,000 was spent on advertising for the Program. The cost to the State of penalties that were waived as part of the Program was approximately $4.0 million relative to what would have been collected if taxpayers had paid without the Program’s penalty forgiveness; the waived interest costs totaled $13.4 million.

The revenue also could have entered State coffers much earlier. As the last tax amnesty period was about ten years prior, if a taxpayer had been waiting for another tax amnesty program, some of these revenues could have conceivably been collected as early as SFY 2017. However, no information is publicly available regarding the length of delay in tax payments from these participating filers.

The new tax filers brought into compliance expands the State’s knowledge of business activity, which will make future compliance easier to achieve through audit work. About 5.8% of the revenue from new filers came through previously-unpaid Interest and Dividends Tax revenue; however, the repeal of that tax means the new information on those taxpayers is of limited future use to the State. New business tax and Meals and Rentals Tax filers can now be tracked in future tax years.

The publicly-available information does not explain why these taxes were unpaid. The high percentage of unpaid taxes from businesses, particularly relative to the SFY 2016 collections, suggests changes in the business tax base may have not been tracked by all taxpaying businesses. While most of the changes in the Business Profits Tax and Business Enterprise Tax since 2016 have reduced revenue to the State, including tax rate reductions resulting in about $1 billion in foregone revenue, some changes could have increased tax liability for certain businesses. For example, changes to business tax law in the previous decade include changes to apportionment, which is the process used to determine which taxable activities are attributable to New Hampshire for multi-state businesses. These changes could have resulted in large, multi-state businesses that sell goods within New Hampshire as well as in other states or countries facing changes in tax liability from apportionment formula shifts that they did not adjust for amongst all the other changes in national and state-level corporate tax law during this period.

Whatever the reasons for past underpayments may have been, State revenues have benefitted substantially from one-time revenues in the Tax Amnesty Program. Legislators should not rely on future programs to generate substantial revenue if they are implemented on a very frequent basis, however. In 2016, the Department of Revenue Administration noted that longer durations between amnesty programs may help generate more revenue through them. There is a risk that people and businesses with overdue taxes may wait to pay them if they expect an amnesty program to be created soon. In addition, the State will forego more interest and penalty payments if these amnesty programs happen with greater regularity and taxpayers wait for a new amnesty program to pay overdue taxes. Policymakers should consider these revenues a one-time windfall that will help the current State Budget fund ongoing services until the next budget takes effect, likely in July 2027.