KEY POINTS

-

- The Medicaid Enhancement Tax (MET) is a 5.4 percent tax on inpatient and outpatient net patient service revenue that each of the state’s 26 acute care hospitals pay during their fiscal year.

- The MET generated approximately $348 million in revenue in SFY 2025, ranking as the fourth-largest state tax revenue source that year.

- MET-supported funding accounted for about one quarter of total Medicaid spending in SFY 2025, including approximately $405 million in federal Medicaid matching funds.

- Disproportionate Share Hospital (DSH) payments help offset uncompensated care and Medicaid reimbursement shortfalls, with payments supporting over a quarter of the cost of care for Medicaid recipients.

- Non-hospital Medicaid providers also receive allocations from the MET, helping offset the General Fund support required for Medicaid provider reimbursement.

- Upcoming federal changes to provider taxes will reduce the MET’s tax base from its current 5.4 percent to 3.5 percent by October 2031, limiting the amount of revenue the MET can collect for health care services.

- If the new 3.5 percent cap was applied to collected MET revenue during SFY 2025, the State would have lost more than $271 million in revenue, including at least $149 million in forgone federal Medicaid matching funds.

- Nearly $1 billion in MET revenue, and at least $1 billion in federal Medicaid match dollars, could be lost by State Fiscal Year 2035 under the federal provider tax changes.

Hospital provider taxes, including the Medicaid Enhancement Tax (MET) in New Hampshire, are long-standing funding mechanisms that have provided significant support for Medicaid programs over the past several decades.[1] The MET is currently a 5.4 percent tax on net patient service revenue (NPSR) from inpatient and outpatient hospital services, paid by all 26 acute care hospitals in the state during their fiscal year. Medicaid, a state-federal fiscal partnership, provides coverage for: adults and children with low incomes, people with disabilities, certain older adults and nursing facility care, pregnant mothers with low incomes, children in foster care or formerly in foster care, and other populations with eligible medical needs and financial eligibility.

Revenue collected from provider taxes allows states to draw down significant federal Medicaid matching funds, which are typically redistributed to Medicaid providers through Medicaid payments. In New Hampshire, the MET raises revenue to help fund Disproportionate Share Hospital (DSH) payments and other Medicaid-directed payments to hospitals, as well as helps support payments to other non-hospital Medicaid providers. These funds help offset uncompensated care paid for by medical service providers, backfill potential lost revenue from lower Medicaid reimbursement rates for providers, and support hospital operations across the state. In State Fiscal Year (SFY) 2025, the MET generated approximately $348 million in revenue, making it the fourth-largest source of State tax revenue for public services. MET-generated funds accounted for more than a quarter of all Medicaid spending in the Granite State during SFY 2024, after federal matching funds were accounted for.

New federal policy changes now threaten the longstanding federal mechanism that has enabled states to raise revenue to support their Medicaid programs. While federal legislation in 1991 initially allowed states to use federally approved provider taxes to help fund their Medicaid programs, recent federal legislation enacted in 2025 freezes existing provider taxes and will gradually lower the maximum allowable provider tax rate for states that adopted Medicaid Expansion, reducing the federal cap from 6.0 percent to 3.5 percent by 2031. While these impacts will not be seen in New Hampshire until October 2028, these changes will ultimately constrain the State’s ability to generate MET revenue and leverage federal Medicaid matching funds. As MET revenue has continued to increase over the past decade, forthcoming federal limits introduce significant uncertainty for the long-term financing of Medicaid services and hospital care across the state.

This Issue Brief examines the history behind New Hampshire’s hospital provider tax, the Medicaid Enhancement Tax (MET), and Disproportionate Share Hospital (DSH) payments, highlighting how hospitals and other Medicaid providers have benefited from these payments over time. This Issue Brief provides insights into upcoming federal changes to provider taxes that will impact the amount of funding available to support health care services in New Hampshire.

What is the Medicaid Enhancement Tax?

Revenue generated through hospital-specific federally authorized provider taxes, or the Medicaid Enhancement Tax (MET) in New Hampshire, is used by 46 states to finance a portion of Medicaid expenditures, thereby drawing down additional federal Medicaid matching funds that are typically returned to providers to support patient care. New Hampshire was among the first states to adopt this funding approach, with all except four states, including Alaska, Delaware, North Dakota, and South Dakota, currently utilizing a provider tax on hospitals.[2] Hospital-specific provider taxes are only a subset of all provider tax policy mechanisms and various other provider taxes are used throughout the country, including taxes on nursing facilities, intermediate care facilities, managed care organizations, and ambulatory services.

The MET is one of two provider taxes used to support Medicaid-funded services in New Hampshire. The Nursing Facility Quality Assessment (NFQA), a 5.5 percent tax on net patient revenue collected from nursing facilities, is crucial for supporting long-term supports and services across the Granite State. Similar to the MET, NFQA revenues are used to leverage additional federal Medicaid funds to support public services.[3] Some national-level analyses also consider the Insurance Premium Tax a provider tax as well, as it can impact the managed care organizations (MCOs) that operate components of Medicaid in the state. A small portion of that tax’s revenue supports the non-federal share for the State’s Medicaid Expansion program. However, while the Insurance Premium Tax can interact with MCOs, it is not solely a provider tax.[4]

The state’s provider taxes have undergone several changes since their enactments, shaped by both federal and state-level policy decisions. While some states began implementing provider taxes as early as the 1980s, the federal Medicaid Voluntary Contribution and Provider Specific Tax Amendments of 1991 established a formal framework for lawful provider taxes and placed limitations on their use for Medicaid programs. In order to receive federal matching funds under the established conditions, provider taxes must be broad-based, uniform, and structured so that providers are not held harmless, meaning that providers are not guaranteed to receive full reimbursement of the tax through Medicaid payments.[5]

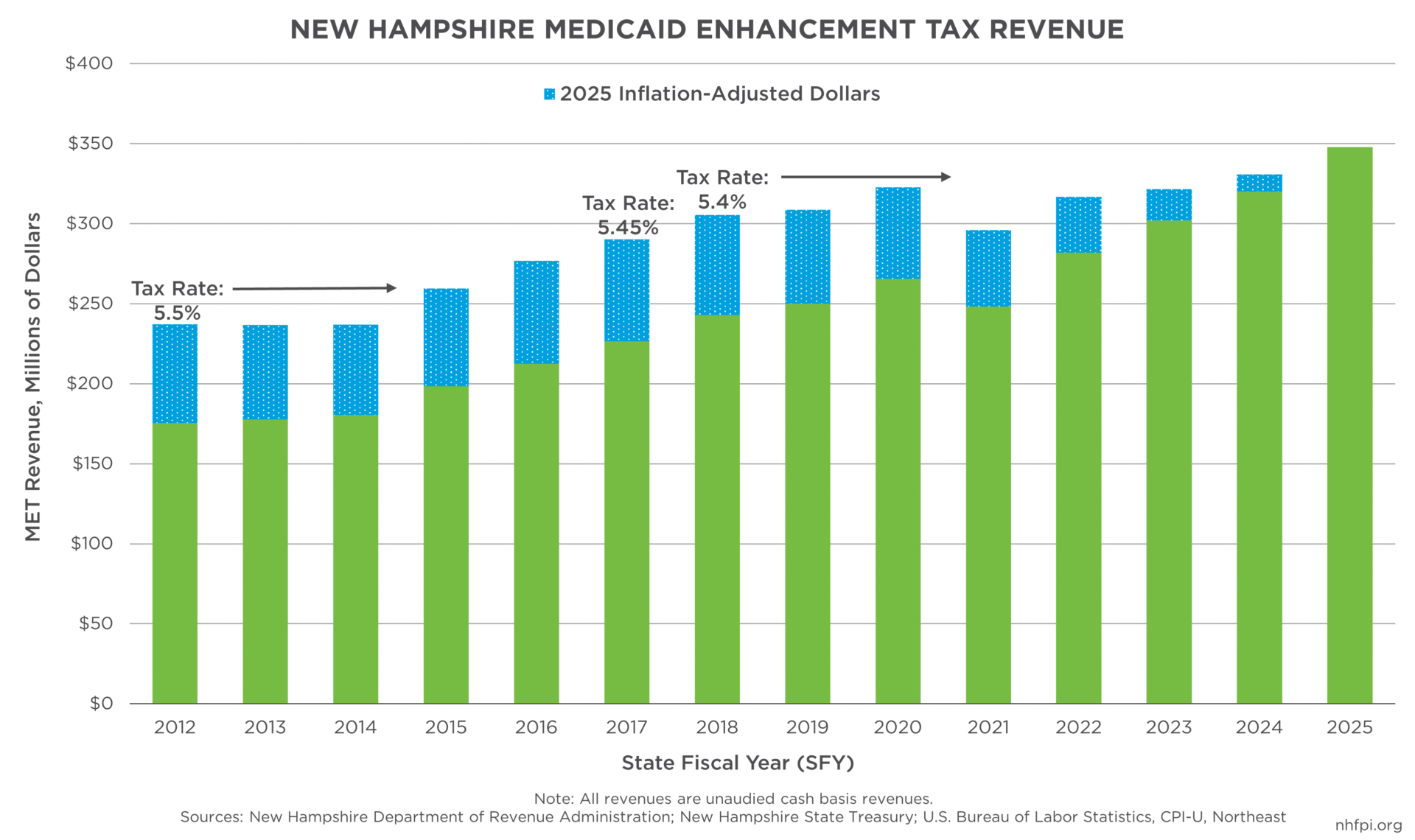

Following the new federal law, New Hampshire formally enacted the MET in 1991, initially implementing a tax equal to 8 percent of a hospital’s gross patient service revenue. By 1995, the tax rate was reduced to 6 percent, and it was further lowered to 5.5 percent in 2007. Over time, the tax base has also shifted from gross revenue to net revenue, reflecting the total amount of money collected by a hospital after accounting for charity care, bad debt, and other deductions from its total billed charges.

Federal audits, changes in federal regulations, and provider legal challenges, as well as the establishment of a statutory formula, or RSA 167:64, for distributing uncompensated care and Medicaid funds in New Hampshire, have resulted in numerous changes to the MET overtime. In 2009, a federal audit challenged New Hampshire’s system of raising dollars and distributing Medicaid payments, with subsequent legal challenges raising questions about the tax’s constitutionality. Rather than eliminating the tax and forgoing associated federal Medicaid matching funds, the legislature modified the statutory provisions and the State and hospitals entered into a negotiated agreement in 2014. Under that agreement, the tax rate was lowered to 5.45 percent in 2016 and to 5.4 percent in 2017. A subsequent six-year agreement adopted in 2018 removed the possibility of further reductions, as the tax had been at risk of falling to 5.25 percent in 2018 if total uncompensated care costs dropped below $375 million. Since that time, the MET has remained set at 5.4 percent of net patient service revenue and continues to serve as a major funding source for funding health care services in New Hampshire.[6]

Over time, the MET has become an increasingly significant contributor to funding public services. In State Fiscal Year (SFY) 2016, the MET generated $212.5 million, which was lower than several other tax revenue sources with similar receipts that year, including the Statewide Education Property Tax ($363.1 million), Meals and Rentals Tax ($313.0 million), Business Enterprise Tax ($272.3 million), and the Tobacco Tax ($227.1 million). By SFY 2025, the MET has grown to $347.8 million, or 10.7 percent of all State tax revenue that year, and surpassed most other tax revenue streams; it was the fourth-largest tax revenue source in the state, behind only the Business Profits Tax (estimated $834.2 million), the Meals and Rentals Tax ($481.9 million), and the Statewide Education Property Tax ($364.4 million).

MET revenues have also shown relatively steady growth over time; from SFY 2016 to SFY 2025, MET revenue declined in only one out of the ten fiscal years, while combined revenues for the General and Education Trust Funds experienced more frequent year-over-year volatility. From SFYs 2016 to 2025, MET revenues have grown, in percentage terms, faster than most of the State’s other major tax revenue sources, rising 63.7 percent compared to 54.3 percent for the Meals and Rentals Tax, 54.1 percent for the Real Estate Transfer Tax, and 51.6 percent for the Insurance Premium Tax. Combined Business Profits Tax and Business Enterprise Tax receipts collectively rose 56.7 percent during this period, although Business Profits Tax revenue alone likely increased substantially faster.[7]

What Are Disproportionate Share Hospital Payments and How Have They Supported Uncompensated Care

MET revenue is paid into an uncompensated care fund and is used to leverage additional federal Medicaid matching funds through Medicaid payments.[8] The uncompensated care fund, established through RSA 167:64, is used to fund a portion of Medicaid payments, including to hospitals as uncompensated care payments or Disproportionate Share Hospital (DSH) payments. DSH payments historically have helped offset the cost of uncompensated care for uninsured patients and support lost revenue associated with care for Medicaid recipients, as Medicaid reimbursement rates are typically lower than those paid by private insurance or Medicare.[9] Formally established under the federal Omnibus Budget Reconciliation Act of 1981, DSH payments have long supported hospital care for Granite Staters.[10] Most Medicaid services in New Hampshire have a 50-50 federal Medicaid match, meaning that for every dollar spent on traditional Medicaid services, the State finances half of the cost, while the federal government funds the other half. Because of this arrangement, New Hampshire has been able to secure a significant amount of federal funding to support services for Granite Staters.

Currently, all 26 acute care hospitals in New Hampshire, including 13 critical access hospitals, receive uncompensated care and other Medicaid payments that are negotiated as part of the overall Medicaid funding and payment program in New Hampshire. New Hampshire Hospital, a State-owned hospital facility providing inpatient psychiatric treatment, also receives funding generated from the MET despite not paying a MET; however, allocations have a different set of regulations and are appropriated directly through the hospital’s State Budget, rather than distributed through DSH payments.[11]

While all hospitals contribute the same percentage of their inpatient and outpatient NPSR towards the MET, the amount each hospital receives back in DSH payments varies and is typically based on factors such as hospital size and the level of uncompensated care provided. Hospitals that serve a higher share of uninsured patients or Medicaid enrollees, and thus face higher uncompensated care burdens, typically have received larger payments.[12] While the majority of MET-supported funds have flowed through DSH payments in prior years, some funds are also distributed through Medicaid rate increases, supplemental payments, and other directed payments, which are typically left to the discretion of the New Hampshire Department of Health and Human Services.[13]

As New Hampshire’s uninsured rate has decreased over time, DSH payments have increasingly been used to offset Medicaid payment shortfalls rather than care for the uninsured. Following the federal Patient Protection and Affordable Care Act of 2010 and the subsequent adoption of Medicaid Expansion by New Hampshire in 2014, the state’s uninsured rate fell by more than half, from approximately 10.7 percent in 2013 to 4.5 percent as of the most recent 2024 data.[14]

According to the Medicaid and CHIP Payment and Access Commission (MACPAC)’s Annual Analysis of Medicaid and Disproportionate Share Hospital Allotments to States, approximately 91 percent of total Medicaid patient costs in New Hampshire’s hospitals in 2019 were covered by either Medicaid reimbursement payments or DSH payments, with DSH payments covering about a quarter, or 26 percent, of the cost of care. Simply put, Medicaid payments likely do not cover all uncompensated care provided at New Hampshire’s hospitals. Because New Hampshire’s Medicaid reimbursement rates are typically lower compared to most other states, offsetting hospital revenue losses associated with Medicaid patients account for a larger share of DSH payments compared to national trends.[15]

Adjustment to DSH Payments Over Time

Prior to 2014, hospitals generally received back the full amount they paid towards the MET. Under changes resulting from federal audits and subsequent legal challenges, hospitals no longer received full reimbursement of their MET payments, with DSH payments tied more directly to uncompensated care costs. Critical access hospitals were reimbursed for approximately 75 percent of their uncompensated care costs, while non-critical access hospitals received payments equal to 50 percent of their uncompensated care costs.[16]

The MET/DSH structure was modified again under a subsequent SFY 2018 agreement, which increased the overall level of DSH payments for non-critical access hospitals.[17] Under these changes, non-critical access hospitals were reimbursed, in aggregate, for 92.2 percent of the MET they paid in SFY 2018, 90.2 percent in SFY 2019, and 86.0 percent in SFYs 2020-2024.[18] While critical access hospitals still received payments equating to about 75 percent of their uncompensated care costs, payment structures were adjusted in SFY 2021; under the new rules, critical access hospitals are reimbursed through managed care organization (MCO) contract allocations and supplemental payments, which provide more flexibility in spending compared to traditional DSH payments.[19]

Following the expiration of the prior agreement in SFY 2025, the State and hospitals entered into another contract to continue DSH payments. While the full details of the agreement are still being finalized and have not yet been made public, the framework for the new contract was enacted into law as Chapter 250, Laws of 2025 after first being introduced as Senate Bill 249 during the 2025 legislative session. Under the new agreement, hospitals will receive payments equal to about 91 percent of their MET contributions, in aggregate. The agreement is scheduled to expire at the end of SFY 2027, at which time a new agreement will likely be required.[20] Under the new agreement, DSH payments also shifted to primarily direct payments to hospital providers, rather than traditional DSH payments through the State Budget’s uncompensated care pool budget line. From SFY 2025 to 2026, budgeted allocations to the hospital uncompensated care pool declined by $223.9 million (91.5 percent), essentially shifting hospital payments outside of these State Budget allocations.[21]

Medicaid Enhancement Tax Revenues and Funding Medicaid Services

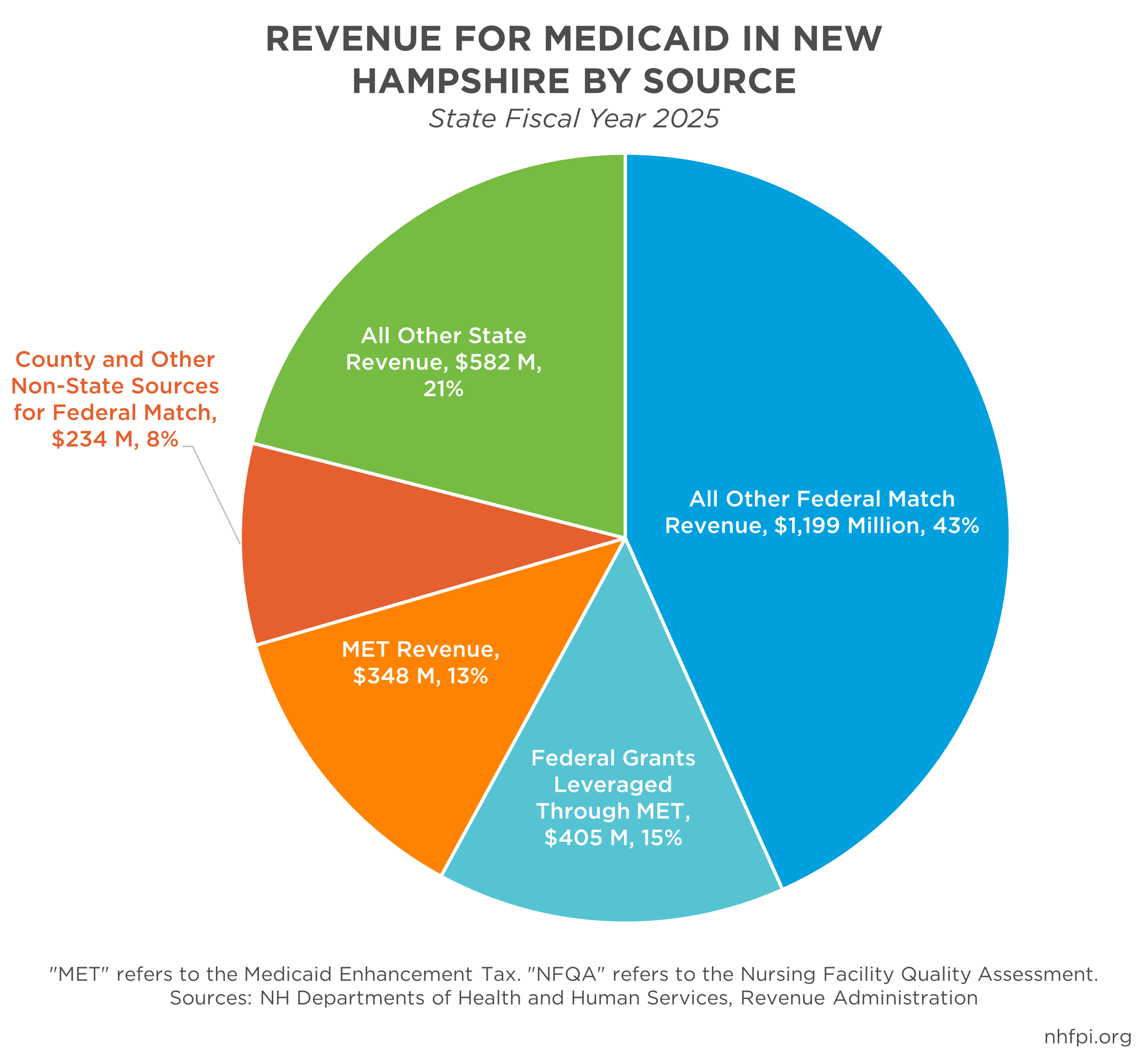

As MET revenue has grown, it has become an increasingly important source of funding for New Hampshire’s Medicaid program. In SFY 2025, approximately $753.5 million (27.2 percent) of the state’s total Medicaid funding was generated through the MET, including about $405.1 million in federal Medicaid matching funds. Approximately 25.3 percent of all federal funds supporting the state’s Medicaid program in SFY 2025 were leveraged through MET collections.[22]

Although hospitals receive back the majority of what they contribute to the MET in aggregate, before accounting for federal match funds, a portion of collected revenue also supports Medicaid payments for non-hospital providers, generally reducing the amount of State General Fund support required to fund the state’s share of Medicaid program costs. Any MET revenue remaining after hospital payments is typically directed toward Medicaid provider payments. In SFY 2025, approximately $450.4 million (59.8 percent) of collected MET revenue and associated federal Medicaid matching funds ($753.5 million total) supported payments for medical providers.[23]

In addition to supporting hospital uncompensated care and MCO payments, a smaller share of MET revenue is deposited into the Granite Advantage Health Care Trust Fund. This off-State Budget fund finances the Granite Advantage Health Care Program, commonly known simply as “Granite Advantage” or Medicaid Expansion here in New Hampshire. This program provides health coverage for Granite Staters with low incomes up to 138 percent of the federal poverty guidelines, or $22,025 for a household of one and $37,702 for a household of three in 2026.[24] As of December 2025, 53,536 people were enrolled in the Granite Advantage program, comprising about a third, or 30.6 percent, of the state’s total Medicaid population.[25]

Since MET revenue deposits into the Granite Advantage Trust Fund began in SFY 2022, a total of $16.6 million in MET revenue has been deposited.[26] The Granite Advantage program yields a higher federal matching rate than traditional Medicaid, with the federal government financing 90 percent of costs, compared with 50 percent under traditional Medicaid. As a result, the deposited MET revenue is estimated to have generated approximately $149.8 million in federal Medicaid matching funds over three fiscal years, providing expanded available funding for the program and likely reducing the amount of General Fund appropriations needed.

Looking Ahead: Upcoming Federal Changes to Provider Taxes

In July 2025, the federal government enacted a new reconciliation law, commonly referred to as the One Big Beautiful Bill Act, which makes significant changes to the Medicaid program, including new restrictions on provider taxes and federal financing. In order to receive federal matching funds under the new law, states are prohibited from enacting new provider taxes or increasing current ones, effectively freezing all provider taxes at their July 2025 levels.

In addition, states that have adopted Medicaid Expansion coverage under the Affordable Care Act, including New Hampshire, will be subject to a gradual reduction in the allowable provider tax cap. Currently set at 6.0 percent at the federal level, the provider tax cap will be reduced to 5.5 percent in October 2027 and further reduced by 0.5 percentage points each year until it reaches a new maximum of 3.5 percent in October 2031. Because New Hampshire’s MET is currently set at 5.4 percent, the State will not experience direct impacts from these reductions until October 2028. This reduction will occur during the SFYs 2028-2029 budget biennium and as the State begins planning for the SFYs 2030-2031 biennium, introducing new fiscal pressures as the State builds its plan to fund public services.

Taxes on nursing facilities and intermediate care facilities, including New Hampshire’s Nursing Facility Quality Assessment, are exempt from the new federal changes. However, reductions in State and federal revenue will likely impact the Medicaid program more broadly, creating challenges for funding services and support for uncompensated care.[27] According to early estimates from the U.S. Congressional Budget Office, the provider tax provisions in the reconciliation law are expected to reduce federal Medicaid spending by $191.1 billion nationwide over ten years.[28] Given that 49 states impose a tax on hospitals (Alaska does not have a hospital provider tax), 22 tax MCOs, and 21 tax ambulatory services, the law is expected to have varying implications for state-level Medicaid programs nationwide.[29] If the MET was capped at 3.5 percent during SFY 2025, rather than its current 5.4 percent tax rate, New Hampshire would have lost at least $270.9 million in MET revenue for Medicaid, including at least $148.5 million in forgone federal matching funds.[30] Of the estimated $2.8 billion expended through the Medicaid program in New Hampshire in SFY 2025, the $270.9 million in lost revenue would represent approximately 9.8 percent of total spending.

If the MET tax base were to grow by 5.5 percent annually, which was the average growth rate from SFYs 2013-2025 and what is projected for SFY 2026, New Hampshire could lose nearly $1.0 billion in MET revenue by SFY 2035 due to the federal provider tax reductions, compared to if those reductions were not going into effect. This would equate to a total of at least $2.0 billion in lost revenue when accounting for associated federal Medicaid matching funds; the amount could be potentially higher for funds used to support Medicaid Expansion and eligible for the 90 percent federal match. Under this same growth assumption, MET revenue collections could generate an estimated $408.4 million by SFY 2028, before declining each year once the federal provider tax changes are implemented in New Hampshire. By SFY 2032, MET revenues could likely reach levels comparable to the $319.9 million collected during SFY 2024.[31] These projections assume continued growth in hospital net patient revenues and the associated MET tax base; however, that growth could slow or stall if other changes to Medicaid increase uncompensated care and further strain hospital finances.

Other Federal Changes to Medicaid

Beyond provider tax restrictions, other Medicaid changes included in the federal law are likely to increase uncompensated care burdens for providers in New Hampshire. By January 2027, adults ages 19-64 enrolled in the Granite Advantage program will be required to comply with new work or community engagement requirements to retain Medicaid coverage, unless they qualify for an exemption. Although about 75 percent of Medicaid enrollees are engaged in the state’s workforce, administrative barriers and documentation challenges could lead to substantial coverage losses.[32] According to early estimates from the Center for Budget and Policy Priorities, up to 22,000 Granite Advantage enrollees, or about 35 percent of the program’s December 2025 population, could lose coverage.[33]

The new federal law also introduces cost-sharing requirements for Granite Advantage enrollees, imposing copayments up to $35 for certain services. For families with very low incomes, these costs could lead to forgone preventive care, potentially increasing reliance on emergency services and the need for uncompensated care. In addition, the law restricts Medicaid eligibility for certain lawfully residing immigrants in the United States, effectively disenrolling some individuals from coverage. Separate from the reconciliation law, the expiration of enhanced premium tax credits for individuals enrolled in Affordable Care Act marketplace plans is also expected to further increase uncompensated care. Nationally, an estimated 4.8 million people are projected to lose health insurance coverage due to the expiration of these credits and higher out-of-pocket costs.[34] While the direct impact of these changes on New Hampshire’s health care system remains uncertain, the combined impact of coverage losses and reduced Medicaid financing is likely to increase uncompensated care and place added financial strain on providers across the state.

New Hampshire’s MET/DSH payment structure faces substantial uncertainty in the State Budget cycles ahead. Recent federal policy changes impose restrictions on provider tax growth and reduce the amount of federal Medicaid funding that states can generate through these mechanisms. Beginning in October 2028, during the next SFYs 2028-2029 budget biennium, the Granite State will be required to reduce the MET tax rate, directly affecting future MET revenue collections and limiting the State’s ability to leverage federal matching funds. In addition, new Medicaid work requirements, cost-sharing provisions, and coverage changes are likely to increase Medicaid coverage losses and uncompensated care, further straining health care finances. Finally, the State and hospitals will have to negotiate a new agreement in this strained fiscal context. As policymakers prepare for upcoming State Budget cycles, close monitoring of federal implementation will be essential to maintaining health care stability and securing access to care.

End Notes

[1] For more information on the MET, see NH RSA 84-A: Medicaid Enhancement Tax.

[2] See The New York Times, G.O.P. Targets a Medicaid Loophole Used by 49 States to Grab Federal Money. For more information on provider taxes and their uses nationally, see the KFF, 5 Key Facts About Medicaid and Provider Taxes, December 2025.

[3] For more information on the NFQA, see NH RSA: 84-C: Nursing Facility Quality Assessment.

[4] To learn more about the Insurance Premium Tax and how the funds are distributed, see the New Hampshire Joint Legislative Fiscal Committee Item FIS 25-226, NHFPI’s Revenue in Review, May 2017, page 20, and NHFPI’s New Hampshire Policy Points 2025 chapter, Funding Public Services. For a national-level analysis that includes the Insurance Premium Tax in provider taxes, see KFF’s States Reporting Taxes by Provider Type, SFY 2025.

[5] For more federal historical information on provider taxes, see the U.S. Congressional Research Service, Medicaid Provider Taxes, updated December 2024, and Medicaid and CHIP Payment and Access Commission (MACPAC), Health Care-Related Taxes in Medicaid, May 2021.

[6] For more information on MET changes in New Hampshire overtime, see the NH Department of Revenue Administration, 2025 Annual Report, page 67.

[7] For all tax receipts, including for the MET, see the NH Department of Revenue Administration’s 2025 Annual Report, page 40, and the New Hampshire Annual Comprehensive Financial Reports (ACFR). For more information on revenue streams, see NHFPI’s New Hampshire Policy Points 2025, Second Edition, Funding for Public Services, and NHFPI’s Revenue and Tax webpage for most recent updates.

[8] For more information on DSH payments, see NH RSA 167:64: Uncompensated Care and Medicaid Fund.

[9] See NHFPI’s 2019 Issue Brief Medicaid Home- and Community-Based Care Service Delivery Limited by Workforce Challenges, endnote 2.

[10] See the U.S. Congressional Research Service, Medicaid Disproportionate Share Hospital Payments, updated November 2023. For more information on current DSH requirements and restrictions, see the U.S. Centers for Medicare and Medicaid Services, Medicaid Disproportionate Share Hospital (DSH) Payments.

[11] See the NH Department of Health and Human Services, Division of Medicaid Services, Budget Briefing Book, page 15.

[12] For more information on specific DSH payments, see the NH Department of Health and Human Services, State Plan Amendment: NH-24-0004. Note that these are estimated DSH payments, not final allocations. Also note that payments to critical access hospitals are not included in this list.

[13] See the NH Department of Health and Human Services, Division of Medicaid Services, Budget Briefing Book, page 15.

[14] See the U.S. Census Bureau, American Community Survey, 1-Year Estimates for 2013 and 2024, Table S2701. For more information on Medicaid Expansion in New Hampshire, see NHFPI’s January 2023 Issue Brief, The Effects of Medicaid Expansion in New Hampshire.

[15] See the Medicaid and CHIP Payment and Access Commission (MACPAC), Annual Analysis of Medicaid Disproportionate Share Hospital Allotments to States, page 67.

[16] See the NH Department of Administrative Services, SFY 2017 Annual Comprehensive Financial Report, page 12.

[17] For more information on the law altering the State and hospital MET/DSH agreement, see House Bill 1817. For more information on New Hampshire’s Mini-Budget of 2018, see NHFPI’s May 2018 blog, Legislature Spends Most of Surplus, Raising Questions for Next Year.

[18] See the NH Department of Revenue Administration, SFY 2018 Comprehensive Annual Financial Report, page 11.

[19] See the NH Department of Health and Human Services, Division of Medicaid Services, Budget Briefing Book, page 15.

[20] For more information on the law altering the State and hospital MET/DSH agreement, see Senate Bill 249.

[21] See the SFYs 2024-2025 State Operating Budget and the SFYs 2026-2027 State Operating Budget.

[22] Total Medicaid expenditure numbers, as well as MET-associated allocations, for SFY 2025 were acquired through the NH Department of Health and Human Services. These calculations assume a 50/50 federal match for revenues raised through the NFQA as reported by the NH Department of Revenue Administration.

[23] Data acquired through the NH Department of Health and Human Services’ Division of Medicaid Services. Payments to hospitals consist of DSH payments, supplemental payments, and directed payments. Payments include combined MET revenue and associated federal Medicaid match funds. SFY 2026 data is projected data and is subject to change; SFYs 2020-2025 data are actual spent amounts.

[24] See the U.S. Department of Health and Human Services, 2026 Poverty Guidelines: 48 Contiguous States.

[25] See the NH Department of Health and Human Services, New Hampshire Medicaid Enrollment: Demographic Trends and Geography, December 2025, page 2.

[26] See the NH Treasury Department, Bond Statement, page 47.

[27] See Georgetown University, McCourt School of Public Policy, Medicaid, CHIP, and Affordable Care Act Marketplace Cuts and Other Health Provisions in the Budget Reconciliation Law, Explained, July 2025.

[28] See the U.S. Congressional Budget Office, Estimated Budgetary Effects of Public Law 119-21, July 2025.

[29] See the Health Management Associates, Annual KFF Survey of State Medicaid Officials, October 2024. Note that New Hampshire was identified as having a tax on MCOs; this is likely referring to the state’s Insurance Premium Tax, rather than a direct provider tax on MCOs.

[30] These calculations assume a 50/50 federal match for revenues raised through the MET and NFQA as reported by the NH Department of Revenue Administration. For the approximate $3.8 million in MET revenue, as reported by the NH Treasury Department, that funds the federal share of Medicaid Expansion, a 90/10 federal match is assumed for these calculations.

[31] MET revenue for SFYs 2013-2025 were taken from the NH Department of Administrative Services’ Annual Reports and Annual Comprehensive Financial Reports. Projected MET revenue for SFY 2026 was acquired through the NH Department of Health and Human Services’ Division of Medicaid Services. Hospital net patient revenues, or the tax base for the MET, has grown by an average of 5.5 percent each year between those SFYs. Calculations were made assuming a continued average 5.5 percent annual growth rate in the tax base, but this growth rate could vary depending on external factors. Rate reductions for SFY 2029 were applied to three quarters of the year’s total, as reductions will occur in October 2028, or about a quarter of the way through SFY 2029.

[32] See KFF’s May 2025 factsheet, Medicaid in New Hampshire.

[33] For a detailed analysis of all changes included in the federal reconciliation law, see NHFPI’s August 2025 Issue Brief, New Federal Reconciliation Law Reduces Taxes, Health Access, and Food Assistance Supports for Granite Staters.

[34] See the Urban Institute, 4.8 Million People Will Lose Coverage in 2026 if Enhanced Premium Tax Credits Expire, September 2025.