The New Hampshire House of Representatives has proposed an additional reduction in the Business Profits Tax (BPT) rate, which would provide little or no tax reduction to most businesses filing BPT returns, and only provide substantial reductions to a small number of businesses with very high profits. Past analysis suggests prior reductions in New Hampshire’s business tax rates have not generated economic activity sufficient to offset revenue losses. Prior rate reductions also did not appear to have produced significant new economic activity distinguishable from underlying economic conditions.

The House passed a reduction of the BPT rate from 7.6 percent to 7.5 percent that would begin in 2023 for most business entities. This change would follow reductions of the BPT in 2016, 2018, 2019, and 2022. Prior to 2016, the BPT rate had been at 8.5 percent since 2001. The BPT is the State’s largest tax revenue source, and is nearly twice as large as the next largest tax revenue source the State collects.

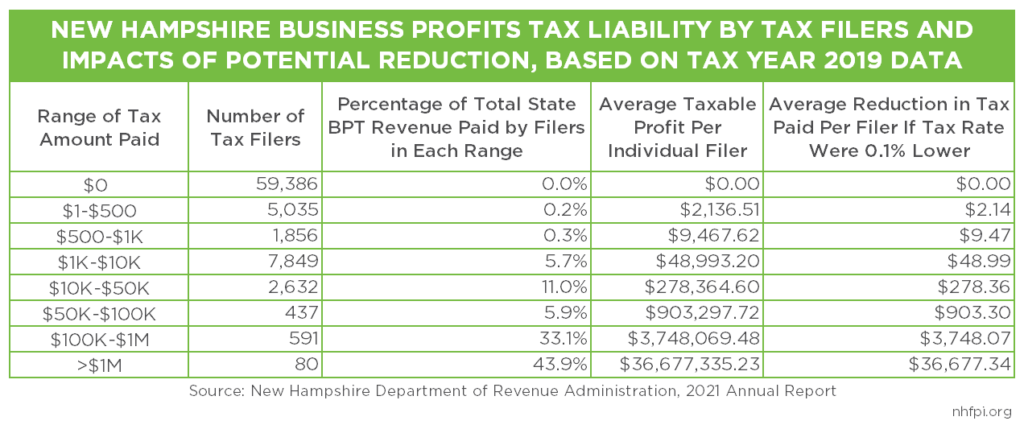

Analysis of data from the New Hampshire Department of Revenue Administration shows a further rate reduction of one tenth of one percent would disproportionately benefit a small number of very profitable entities, with most businesses paying BPT receiving a relatively small tax reduction. In 2019, the most recent year for which there are published data, 80 filers paid 43.9 percent of the BPT revenue collected by the State. Less than 0.9 percent of filers paid about 77.0 percent of the State’s BPT revenue in 2019. About 76.3 percent of filers paid $0 in BPT, likely in large part because they paid the Business Enterprise Tax (BET) and were able to use the BET paid as a credit against any BPT liability they had.

If the tax rate had been 0.1 percent lower for Tax Year 2019, the top 80 filers would have seen an average tax reduction of $36,677.34, which is approximately $10,000 less than the annual wages paid to an employee working 40 hours per week and 52 weeks per year at the estimated median wage in New Hampshire in June 2021. Smaller businesses with lower tax liabilities would have seen more limited reductions. In the most common categorization of profitable filers paying BPT, the 7,849 businesses paying between $1,000 and $10,000 in BPT during 2019, the average tax reduction would have been about $49 per business.

A reduced tax rate would also provide the greatest average tax reduction to large, multistate entities with significant overseas operations. The Department of Revenue Administration’s published data do not reveal where entities filing BPT are headquartered, so any entity may be based in another state, or another country, and only have tax liability in New Hampshire due to a combination of sales, property, or personnel in New Hampshire. The New Hampshire Department of Revenue Administration does not definitively determine where a company is “based” with the information provided in a tax return, including the type of entity or combined entity used in the business tax filing.

One group of filers, called “Water’s Edge” filers, includes multi-part businesses, such as filers with significant overseas operations, that are required to file as one business entity. These combined entities accounted for 5.7 percent of all BPT filers in 2019, but paid 60.2 percent of all revenue collected. With a rate 0.1 percent lower in 2019, Water’s Edge filers would have seen the largest average tax reduction of any group, at $903.90 per filer. Entities filing as Partnerships would have seen an average tax reduction of $80.67, while businesses filing as Corporations would have had an average tax reduction of $45.75. Proprietors, which were the largest group and accounted for 40.4 percent of filers, would have seen an average tax reduction of $7.58.

Past New Hampshire business tax reductions do not appear to have spurred significant new economic growth, including economic growth substantial enough to offset the revenue lost due to tax rate reductions. NHFPI analysis conducted in 2019 examining prior State business tax reductions found no evidence that those policy changes generated sufficient economic growth to generate revenue increases, and little evidence these rate changes impacted economic and job growth overall. Exogenous factors, including historically high national corporate profits, appear to be driving the current rise in BPT revenues, and will likely behave largely independently of policy decisions in New Hampshire. Analysis from the Urban Institute showed New England states overall saw a 36.5 percent increase in corporate tax revenue from the third quarter of 2020 to the same quarter in 2021. New Hampshire’s corporate tax revenues increased as well, but at 26.4 percent, growth in New Hampshire lagged the overall change in New England across those two specific periods.

Analysis from the U.S. Congressional Budget Office both before and during the pandemic, as well as repeated analysis from Moody’s Analytics, suggest that reductions to national corporate income taxes have very limited benefits to economic growth relative to other policies. In a January 2021 analysis projecting across calendar year 2021, Moody’s Analytics estimated every dollar in lost public revenue spent reducing the corporate tax rate would have generated $0.32 of economic growth as measured by the change in U.S. Gross Domestic Product, and permitting businesses to offset their tax liabilities with carried net operating losses on their tax returns would have generated $0.24 in economic growth per every $1.00 in lost public revenue. In contrast, boosting food assistance to households with low incomes would have generated $1.61 for every dollar invested, and supplementing unemployment insurance would have led to a $1.49 boost to the size of the economy for every $1.00 invested. Estimates from other research also suggest food assistance, unemployment compensation, and assistance to households with children and low incomes have much stronger stimulative effects on the economy overall.

The New Hampshire Department of Revenue Administration estimated that the proposed reduction in the BPT rate would cost the State a total of approximately $17.5 million in revenue combined during State Fiscal Years 2023, 2024, and 2025, with an ongoing loss of about $8.4 million per year after 2025. With about one in four Granite State adults reporting in March 2022 that paying for usual household expenses continues to be somewhat or very difficult, public resources must be carefully deployed to help ensure an equitable, sustainable, and inclusive economic recovery.

– Phil Sletten, Senior Policy Analyst

Note: The description of “Water’s Edge” filers was refined to incorporate other combined reporting domestic filers on November 1, 2023.