The Earned Income Tax Credit (EITC), established in 1975, provides assistance to working individuals and families with low incomes. In 1997, the Child Tax Credit (CTC) was enacted to provide additional assistance to families with children. These programs provided significant financial relief to individuals and families, in the form of refundable and non-refundable tax credits, before and during the COVID-19 pandemic. Both were meaningfully expanded and modified by the passage of the American Rescue Plan Act (ARPA) for tax year 2021.

The EITC and the CTC can reduce poverty, improve economic stability and mobility, and support the health and overall outcomes of children, especially among recipients with lower incomes. By design, the EITC incentivizes employment and work as the credit amount increases as earned income rises, then declines once passing a certain point. The credit amount for the CTC also gradually scales down once income grows beyond a certain threshold.

Despite the availability of these credits to many people in New Hampshire, several groups were ineligible to receive support prior to the temporary changes implemented for the 2021 tax year. Many individuals and families with lower incomes were excluded from receiving any EITC dollars, particularly workers aged 19 to 24 and 65 and older without qualifying children. There were also eligibility restrictions for the CTC that excluded filers from being able to claim 17-year-old children for the credit.

Both the EITC and the CTC provide direct resources to Granite Staters and bolster local economies. However, prior to the pandemic, nearly one in five likely eligible Granite Staters did not claim the EITC, and filers representing an estimated 7,745 children who were eligible for CTC did not claim the credit. While the temporary changes to the EITC and CTC expanded eligibility and benefits for those with lower and moderate incomes, additional investments in connecting likely eligible filers with information about these resources, tax preparation assistance, and general outreach may improve program participation as well as support the ongoing economic recovery.

This Issue Brief provides an overview of the EITC and the CTC, including summaries of program eligibility, participation, and economic impacts. Additionally, this Issue Brief covers the key temporary changes to both the EITC and CTC for tax year 2021. This analysis also outlines the overall benefits of these changes in improving the economic stability of individuals and families to help support an equitable and inclusive economic recovery from the COVID-19 pandemic.

Tax Credits as Economic Support and Stimulus

The EITC and the CTC are federal tax credits, which provide support to eligible tax filers in the form of federal tax liability relief. These programs account for a variety of factors when determining eligibility and calculating the amount of tax relief received. This relief is offered through either refundable tax credits or non-refundable tax credits. Refundable tax credits reduce a filer’s federal tax liability by the credited amount, with any remaining credit refunded to the filer in the form of a tax refund, usually arriving as a check or a deposit in the filer’s bank account. Non-refundable tax credits reduce a filer’s federal income tax liability until there is no liability, but any remaining credit balance is not refunded.[i]

Non-refundable tax credits may provide greater benefit for filers with higher incomes, as those filers are more likely to have larger tax liabilities that could be significantly reduced by non-refundable credits. Refundable credits can be more meaningful to filers with lower and more moderate incomes, who may not owe any income tax. In addition to supporting and providing relief to filers, certain tax credits have been shown to help improve economic stability and mobility, especially among filers with lower incomes, and provide meaningful economic stimulus, particularly when the economy is weak.[ii]

During times of economic recovery and growth, extending expanded tax credits directly supported individuals and families while providing economic stimulus. Analysis from 2011 and 2015 from the U.S. Congressional Budget Office found that investments into temporary expansions of transfer payments to individuals, including expanding refundable tax credits, may have resulted in significant economic benefits and increased employment during the recovery from the Great Recession.[iii]

The Earned Income Tax Credit

The federal EITC is a refundable tax credit designed to provide support to employed people with relatively low incomes. Since the program’s inception in 1975, the EITC has been aiding families in paying for expenses while incentivizing work.[iv] The EITC is associated with improvements to the overall health and development of children as well as their long-term outcomes. The EITC also reduces poverty by incentivizing and rewarding work through supplementing the wages of low-income workers.[v]

Notably, support provided by the EITC has been concentrated among households with children. The program’s framework, prior to the temporary expansions in 2021, resulted in nearly all credit dollars assisting households with children; nationally, nearly 97 percent of EITC dollars were disbursed to households that included children during tax year 2020. The program’s structure left many lower income filers without qualifying children able to claim only a very small credit.[vi] Additional data for tax year 2020 show that 67,000 filers in New Hampshire claimed the EITC, resulting in a total of approximately $130 million dollars in refundable tax credits brought into the state. For tax year 2020 in New Hampshire, the average EITC amount paid was $1,950.[vii] The latest available EITC participation data show that in tax year 2018, an estimated 18.2 percent of likely eligible filers did not claim the EITC on their tax returns.[viii] The EITC does not count against resource limits used to determine income eligibility for key federally-funded support programs, such as the Supplemental Nutrition Assistance Program, Medicaid, Supplemental Security Income, or Temporary Assistance for Needy Families.[ix]

Overview of the EITC Immediately Prior to the 2021 Expansions

Eligibility for the EITC and the size of the tax credit is dependent on several conditions, including the filer’s age, marital status, the number of children in the household, income from other sources such as investments, and other factors. The credit grows as an individual’s earned income increases up to a certain threshold, after which the credit tapers off until the upper income limit is met.

To be eligible, the taxpayer must have filed a federal tax return, have a valid Social Security Number, be a citizen or resident alien of the United States, and have an earned income of greater than zero dollars. For tax year 2020, a filer must have had earnings from investment income below $3,650, and total income below a threshold based on the number of qualifying children they have and the filer’s marital status. Filers who did not have qualifying children were only eligible to claim the EITC if they were between the ages of 25 years and 64 years. Qualifying children encompass individuals related to the tax filer, such as a daughter, son, stepchild, foster child, younger brother or sister, or certain other relatives who also share a primary residence with the tax filer. Qualifying children also include full-time students up to age 24 and adults under a certain disability status. Additionally, filers are ineligible to claim the EITC if they have made a fraudulent claim, where they remain ineligible to claim the credit for a period of ten years.[x]

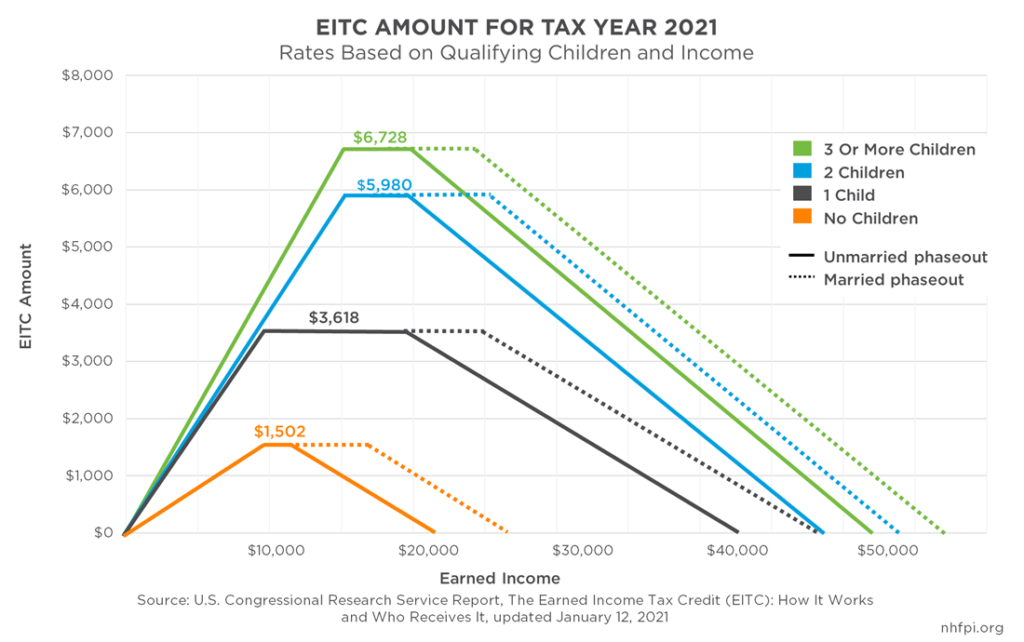

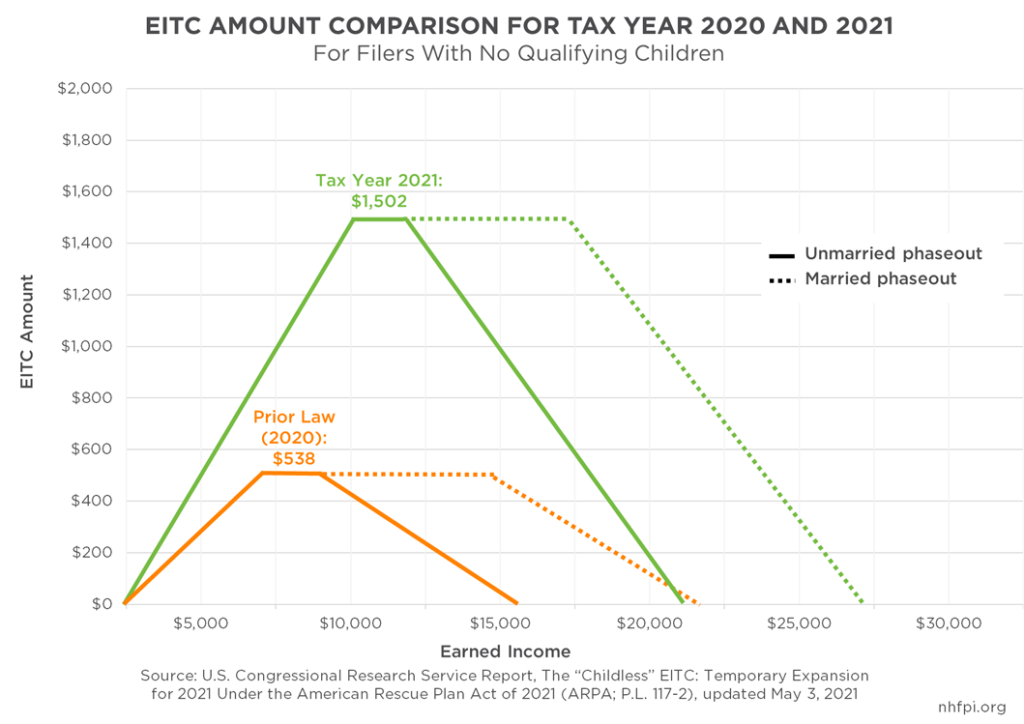

The credit is provided to filers once a year after filing for federal income tax returns and is calculated as a percentage of the amount of earned income from employment. The EITC applies in different percentages, called credit rates, based on a filer’s household composition and income. Phaseout limits, which are the amounts of earned income at which the size of the credit begins to diminish, are dependent on marital status and the presence or number of qualifying children. For tax year 2020, eligible filers without qualifying children claimed on their returns could only claim a very small EITC, with a maximum credit of $538 dollars, whereas a single eligible filer with one child could claim up to a maximum credit of $3,584.[xi]

Income limits exist for claiming the EITC as well. For tax year 2020, an unmarried filer with no qualifying children would only be able to claim the relatively small maximum credit allowed to them if their earned income was below $15,820. However, if they claimed one dependent child, their maximum earned income amount to receive the credit would have been $41,756. The latest pre-pandemic data show that nationally, the most tax returns claiming the EITC were from filers claiming one dependent child, while 39 percent of total EITC dollars went to households claiming two children. Nationwide, only three percent of EITC assistance was received by taxpayers without qualifying children in 2020, likely due to the very low maximum income thresholds relative to such filers and the low maximum amount of the credit available to filers who did not have qualifying children.[xii]

Key Temporary Changes and Expansions to the EITC in 2021

The American Rescue Plan Act expanded the EITC in several key ways for tax year 2021. These changes included broadening program eligibility to include a greater age range of filers, as well as significantly improving benefits, especially for filers who do not have qualifying children. For 2021, individuals aged 19 to 24 years or 65 years or older without qualifying children are eligible for EITC (except for students under age 24), whereas prior law only permitted eligibility among such workers aged 25 to 64 years. Additionally, 18-year-old individuals aging out of the foster system are eligible.[xiii]

The expanded EITC in 2021 also increased the maximum payment for workers without qualifying children who live with them from $543 to $1,502, and set a higher income phaseout of $21,430 for single filers.[xiv] Additionally, the eligibility threshold for income earnings from investment income increased to $10,000, and taxpayers without a Social Security Number may claim the credit under the same eligibility guidelines as EITC filers without qualifying children in 2021.[xv]

Positive Impacts of the Temporary Expansions to the EITC

The expansions of the EITC for tax year 2021 will broaden eligibility, allowing more working individuals in New Hampshire to claim the credit and receive the economic support provided by it, while continuing to incentivize work. A key expansion of the program centers around broadening EITC eligibility for adults without qualifying children. Nationally, workers employed in industries that tend to pay lower wages, including individuals working as cashiers, retail salespersons, food workers, child care workers, laborers, and health aid workers, are the most likely to benefit from the expanded childless EITC. Additionally, national data show that the expanded childless EITC will more equitably support individuals who identify as a race or ethnicity that is not white and non-Hispanic, as many of these individuals disproportionally worked in industries paying lower than average wages.[xvi]

According to a preliminary, unpublished analysis of data from the Joint Committee on Taxation and the U.S. Census Bureau by the Center on Budget and Policy Priorities, the expansion of the childless EITC under ARPA may result in an estimated 66,400 additional Granite Staters receiving tax relief.[xvii] Analysis conducted by the Institute on Taxation and Economic Policy estimated that about 18,000 of the newly-eligible Granite Staters would be young adult workers under the age of 24 with lower incomes, the equivalent of about 29 percent of all young adults in New Hampshire.[xviii]

In January 2021, Moody’s Analytics published an analysis projecting the amount of economic growth by the last quarter of 2021 resulting from a set of federal spending or revenue policy changes in the first quarter of 2021. This analysis estimated that each additional dollar of EITC paid in the first quarter of 2021 would produce a $1.27 boost in economic output nationally in the fourth quarter of 2021. This analysis indicates that the additional Granite Staters eligible for the EITC would not only be supported directly by these credits, but the expanded EITC would also support the ongoing economic recovery and expansion in New Hampshire.[xix]

The Child Tax Credit

First enacted in 1997, the CTC is a tax credit that may be claimed by eligible filers with qualifying children. Prior to the temporary changes enacted for tax year 2021, the CTC was not a completely refundable credit. The CTC itself was a non-refundable credit, with another portion of the credit, called the Additional Child Tax Credit (ACTC), being refundable.[xx]

Despite not being fully refundable prior to the changes for tax year 2021, the CTC has been shown to reduce poverty for both children and adults. Nationally, in 2018, about 4.3 million people were lifted out of poverty by the CTC, including 2.3 million children. An additional 12 million people in poverty nationally experienced less severe poverty as a result of the CTC. Additional research shows that the CTC is associated with improvements in child development and health, school performance, and earnings in adulthood.[xxi]

The program guidelines and structure prior to tax year 2021 limited the refundability of the CTC, disproportionately benefitting filers with higher incomes relative to those with very low or no tax liability. Nationally and in New Hampshire, most children were eligible for this support through the CTC, and a majority of the credit’s dollars were received by taxpayers with incomes between $50,000 and $500,000 per year. For tax year 2019, the average tax credit amount was $2,370, and the largest credits on average were received by households with incomes between $100,000 and $200,000, with smaller average credits for families with lower incomes.[xxii]

Prior to the pandemic, the U.S. Internal Revenue Service estimated that 7,745 children in New Hampshire who were eligible for the CTC in 2019 were not claimed on a tax return for their household.[xxiii] Like the EITC, the CTC does not count against resource limits used to determine income eligibility for key federally-funded support programs, including the Supplemental Nutrition Assistance Program, Medicaid, Supplemental Security Income, or Temporary Assistance for Needy Families.[xxiv]

Overview of the CTC Immediately Prior to the 2021 Expansions

Much like the EITC, the CTC factors the number of qualifying children and a filer’s income into the tax credit calculation. However, income phaseouts for the CTC were much higher than for the EITC, and filers must have had at least $2,500 in earned income during 2020. For tax year 2020, qualifying children were defined as being under the age of 17 by the end of the tax year. Additionally, the child must be the tax filer’s son, daughter, grandson, granddaughter, stepson, stepdaughter, niece or nephew, or an eligible foster child. The child must also live at the same address as the filer for more than half the year, and the child must receive more than half of their support from the tax filer.[xxv]

For tax year 2020, filers with qualifying children received the non-refundable CTC of $2,000 per child under age 17. The refundable compliment of the CTC, the ACTC, was calculated to equal 15 percent of a filer’s earned income over $2,500, totaling no more than a $1,400 refund per child. The phaseout threshold for the CTC began at $200,000 per year for single filers and $400,000 per year for married filers, and the actual phase out rate was dependent on the number of qualifying children.[xxvi]

Key Temporary Changes and Expansions to the CTC in 2021

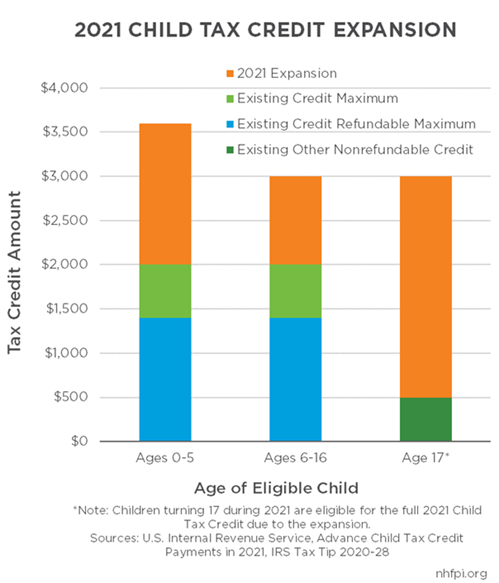

Temporary changes to the CTC for tax year 2021 include boosting total benefits, expanding eligibility, making the credit fully refundable, eliminating the ACTC phase-in cap of $1,400, and providing advance payments of portions of the credit. Compared to 2020, the maximum benefit increased to $3,000, from the previous $2,000 for children ages six to 16 years and from $2,000 to $3,600 for children aged five years and younger. Additionally, in 2020, children who were 17 years old were only eligible under a smaller program that provided a $500 credit, but for tax year 2021, eligibility was extended to include these 17-year-old children, triggering eligibility for a credit of $3,000.[xxvii]

For tax year 2021, the credit was made fully refundable, which increased the benefits received by families with lower incomes who may not have outstanding tax liabilities. Notably, the expanded credit can be received in full by eligible families regardless of income or tax liability, boosting the credit amount for filers with little or no income, and for many families with moderate incomes as well.[xxviii]

Additionally, half of the credit was distributed to families on a monthly basis throughout 2021; payments were distributed automatically based on their eligibility information from 2020. For these filers that received advance payments, the remainder of the credit will be disbursed after they file their 2021 taxes to offset any outstanding tax liabilities or to be included in a tax refund.[xxix]

Positive Impacts of the Temporary Expansions to the CTC

The key changes to the CTC for tax year 2021 boosts the amount of support available to many individuals and families across New Hampshire, and full refundability of the credit will allow for more equitable distributions of tax relief resources.[xxx] The U.S. Congressional Research Service estimated that the expansion’s benefit would be most significant for families in poverty, with the average CTC increasing from $976 to $5,421; increases for higher-income households were estimated to be much smaller.[xxxi]

Advance payments of half of the CTC provided additional support during the second half of the 2021 calendar year, while still allowing for the remainder of the credit to be claimed when tax year 2021 returns are filed. These advance payments provided portions of the credit over a longer timeline, rather than the traditional one-time credit after filing a tax return, allowing more flexibility for families to afford key expenses throughout the year. In New Hampshire, an estimated 75 percent of households with incomes below $35,000 utilized their advance CTC payments for basic needs, such as housing, utilities, education, and food, during mid-2021.[xxxii] Even though expanded CTC benefits were sent to people that the U.S Internal Revenue Service determined to be eligible on a monthly basis in the second half of 2021 without action, the recipient still needs to claim the CTC on their 2021 tax return to access the remaining half of the credit that was not previously distributed on that monthly basis, as well as to avoid the risk of recoupment.[xxxiii]

Estimates from the Center on Budget and Policy Priorities and the Urban Institute suggest that about 8,000 to 11,000 children, respectively, would be lifted out of poverty in New Hampshire if the expansion were to be made permanent, and about 52,000 children under age 17 in New Hampshire would now qualify who previously were ineligible for the full $2,000 credit. The Center on Budget and Policy Priorities calculated that approximately 85 percent of New Hampshire children, or approximately 221,000 children, would benefit from the CTC expansion if made permanent beyond 2021, and that child poverty would be reduced by 39 percent in the state.[xxxiv] During 2021, advance payments of the CTC reached 133,000 filers in New Hampshire, benefitting households with 217,000 children. The average advance CTC monthly payment amount in the state was $414. From July through December 2021, approximately $320,664,000 has flowed into the state due to the CTC through these monthly payments.[xxxv]

Analysis from Moody’s Analytics, published in January 2021, projected the amount of economic growth by the last quarter of 2021 resulting from the CTC policy change in ARPA. This analysis estimated that each additional CTC dollar paid in the first quarter of 2021 would produce a $1.25 boost in economic output nationally in the fourth quarter of 2021.[xxxvi] This analysis suggests additional CTC dollars flowing to Granite Staters can both directly support more children and their families to a greater extent and benefit the overall economic recovery in the state.

Opportunities to Enhance Participation and Support the Recovery

The temporary expansions to both the EITC and the CTC have made tremendous positive impacts to the individuals and families receiving, or set to receive, this increased relief. While the EITC and the non-advance CTC payment will be distributed when taxpayers file their 2021 taxes in 2022, the advance CTC payments received by many eligible families have already provided significant, immediate relief to many Granite Staters during 2021. Estimates from the U.S. Census Bureau’s Household Pulse Survey analyzed by the Center on Budget and Policy Priorities found that a significant portion of these advance payments were used to cover key expenses like housing, utilities, education, and food during mid-2021. In New Hampshire, an estimated 75 percent of households with incomes below $35,000 utilized their advance CTC payments for these basic needs.[xxxvii]

The advance CTC payments of half of the credit were distributed to filers who were identified as eligible based on information held on file by the U.S. Internal Revenue Service from the previous year. In order to receive the remaining portion of the CTC, filers must claim them on their tax returns. In addition to claiming the CTC to receive the remaining amount of relief, filers must also report the advance payments they received in order to avoid the potential recoupment of these credits.[xxxviii] The EITC must also be claimed when filing 2021 taxes in order to receive this relief.[xxxix]

Prior to these expansions, nearly one in five likely eligible Granite Staters did not claim the EITC, and approximately 7,745 children were estimated to be eligible for the CTC while the credit was not claimed on their household’s tax return. The potential under enrollment in key assistance programs, along with underutilization of the EITC and CTC in prior years, suggests there is the opportunity to support public benefit navigators and tax assistance programs to help ensure eligible Granite Staters claim this tax relief, especially given the temporary changes in eligibility and expansions to encompass more lower-income filers for tax year 2021.[xl] Helping ensure that more eligible Granite Staters are able to claim this temporarily expanded tax relief would benefit everyone in the state. The EITC and the CTC provide significant resources and support to individuals and families, while bringing millions of dollars back into the state’s economy to help build a more equitable and inclusive recovery.

Endnotes

[i] Additional information on refundable and non-refundable tax credits is discussed in the Tax Policy Center Briefing Book.

[ii] See the Center on Budget and Policy Priorities July 23, 2015 report New Research: EITC Boosts Employment; Lifts Many More Out of Poverty Than Previously Thought, the October 1, 2015 report EITC and Child Tax Credit Promote Work, Reduce Poverty, and Support Children’s Development, Research Finds, and the May 24, 2016 publication Chart Book: The Earned Income Tax Credit and Child Tax Credit.

[iii] See the U.S. Congressional Budget Office November 15, 2011 testimony titled Policies for Increasing Economic Growth and

Employment in 2012 and 2013 and report titled Estimated Impact of the American Recovery and Reinvestment Act on Employment and Economic Output in 2014 published in February 2015.

[iv] See the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[v] An overview of the positive economic and health outcomes attributed to the Earned Income Tax Credit are discussed in the Center on Budget and Policy Priorities, Policy Basics: The Earned Income Tax Credit.

[vi] See the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[vii] See the U.S. Internal Revenue Service Statistics for Tax Returns with the Earned Income Tax Credit (EITC).

[viii] See the U.S. Internal Revenue Service EITC Participation Rate by States Tax Years 2011 through 2018.

[ix] See the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[x] Information on eligibility for tax year 2020 are published in the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[xi] EITC calculations and disbursement guidelines for tax year 2020 are published in the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[xii] Information on income limits for the EITC for tax year 2020, and pre-pandemic statistics on tax returns are published in the U.S. Congressional Research Service report titled The Earned Income Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[xiii] For more information, see the U.S. Congressional Research Service’s May 3, 2021 report The “Childless” EITC: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2).

[xiv] For more information, see the U.S. Congressional Research Service’s May 3, 2021 report The “Childless” EITC: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2). See also the Center on Budget and Policy Priorities March 12, 2021 report American Rescue Plan Act Includes Critical Expansions of Child Tax Credit and EITC.

[xv] See the U.S. Internal Revenue Service fact sheet IRS: Expanded Credits for Families Highlight Tax Changes for 2021; Many People Who Don’t Normally File Should File This Year, updated February 9, 2022.

[xvi] See the Center on Budget and Policy Priorities May 24, 2021 report Congress Should Adopt American Families Plan’s Permanent Expansions of Child Tax Credit and EITC, Make Additional Provisions Permanent.

[xvii] Dollar value estimate provided by email to NHFPI by the Center on Budget and Policy Priorities. See the Center on Budget and Policy Priorities May 24, 2021 report Congress Should Adopt American Families Plan’s Permanent Expansions of Child Tax Credit and EITC, Make Additional Provisions Permanent.

[xviii] See the Institute on Taxation and Economic Policy February 8, 2022 report Federal EITC Enhancements Help More Than One in Three Young Workers.

[xix] See the Moody’s Analytics January 15, 2021 publication The Biden Fiscal Rescue Package: Light on the Horizon.

[xx] See the U.S. Congressional Research Service report titled The Child Tax Credit: How It Works and Who Receives It, updated January 12, 2021, and The Child Tax Credit: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2), updated May 12, 2021. See also the Center on Budget and Policy Priorities October 1, 2015 report EITC and Child Tax Credit Promote Work, Reduce Poverty, and Support Children’s Development, Research Finds.

[xxi] The positive economic and health outcomes attributed to the Child Tax Credit are discussed in the Center on Budget and Policy Priorities, Policy Basics: The Child Tax Credit.

[xxii] Information on eligibility for tax year 2020 and statistics on filers and credit amounts are published in the U.S. Congressional Research Service report titled The Child Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[xxiii] For the full dataset, including analysis by ZIP code, see the U.S. Internal Revenue Service’s web page 2021 Child Tax Credit and Advance Child Tax Credit Payments: Resources and Guidance.

[xxiv] See the U.S. Congressional Research Service report titled The Child Tax Credit: How It Works and Who Receives It, updated January 12, 2021.

[xxv] Information on eligibility for tax year 2020 are published in the U.S. Congressional Research Service report titled The Child Credit: How It Works and Who Receives It, updated January 12, 2021.

[xxvi] CTC calculations and disbursement guidelines for tax year 2020 are published in the U.S. Congressional Research Service report titled The Child Credit: How It Works and Who Receives It, updated January 12, 2021.

[xxvii] For comparisons to prior tax law, see the U.S. Internal Revenue Service Publication 972, Child Tax Credit and Credit for Other Dependents, for 2020 Returns, published January 11, 2021 and the U.S. Congressional Research Service report titled The Child Tax Credit: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2), updated May 12, 2021.

[xxviii] To learn more about the Child Tax Credit expansion, see the U.S. Internal Revenue Service, Looking Ahead: How the American Rescue Plan Affects 2021 Taxes, Part 2 (COVID Tax Tip 2021-79), June 3, 2021. See also NHFPI’s May 19, 2021 webinar presentation Federal Aid and the Recovery from the COVID-19 Crisis, NHFPI’s March 26, 2021 blog post Federal American Rescue Plan Act Directs Aid to Lower-Income Children, Unemployed Workers, and Public Services, the U.S. Congressional Research Service’s May 12, 2021 report The Child Tax Credit: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2), and the U.S. Congressional Research Service’s July 13, 2021 report The Child Tax Credit: The Impact of the American Rescue Plan Act (ARPA; P.L. 117-2) Expansion on Income and Poverty.

[xxix] See the U.S. Congressional Research Service report titled The Child Tax Credit: Temporary Expansion for 2021 Under the American Rescue Plan Act of 2021 (ARPA; P.L. 117-2), updated May 12, 2021.

[xxx] See the Center on Budget and Policy Priorities May 24, 2021 report Congress Should Adopt American Families Plan’s Permanent Expansions of Child Tax Credit and EITC, Make Additional Provisions Permanent.

[xxxi] For the full research findings, see the U.S. Congressional Research Service’s July 13, 2021 blog The Child Tax Credit: The Impact of the American Rescue Plan Act (ARPA; P.L. 117-2) Expansion on Income and Poverty.

[xxxii] See the Center on Budget and Policy Priorities October 21, 2021 report 9 in 10 Families With Low Incomes Are Using Child Tax Credits to Pay for Necessities, Education.

[xxxiii] For additional information on the structure of the Child Tax Credit, see the U.S. Internal Revenue Service’s web pages Advance Child Tax Credit Payments in 2021 and 2021 Child Tax Credit and Advance Child Tax Credit Payments Frequently Asked Questions.

[xxxiv] For the Urban Institute analysis estimating 11,000 children would be lifted out of poverty in New Hampshire by extending the current Child Tax Credit expansion, see the August 2021 report Expanding the Child Tax Credit Could Lift Millions of Children Out of Poverty. For the Center on Budget and Policy Priorities estimate of 8,000 New Hampshire children being lifted out of poverty by an extended expansion of the Child Tax Credit, see the May 24, 2021 report Congress Should Adopt American Families Plan’s Permanent Expansions of Child Tax Credit and EITC, Make Additional Provisions Permanent.

[xxxv] See the Department of the Treasury December 15, 2021 report By State: Advance Child Tax Credit Payments Distributed in December 2021.

[xxxvi] See the Moody’s Analytics January 15, 2021 publication The Biden Fiscal Rescue Package: Light on the Horizon. Moody’s analyzed ARPA policies as proposed in January 2021, before the March 2021 package passed.

[xxxvii] See the Center on Budget and Policy Priorities October 21, 2021 report 9 in 10 Families With Low Incomes Are Using Child Tax Credits to Pay for Necessities, Education.

[xxxviii] For additional information on the structure of the Child Tax Credit, see the U.S. Internal Revenue Service’s web pages Advance Child Tax Credit Payments in 2021 and 2021 Child Tax Credit and Advance Child Tax Credit Payments Frequently Asked Questions.

[xxxix] For more information on the Earned Income Tax Credit, see the U.S. Internal Revenue Service’s web page A Closer Look at the Earned Income Tax Credit.

[xl] See NHFPI’s October 7, 2021 Issue Brief The Supplemental Nutrition Assistance Program: State Outreach to Eligible Populations, December 16, 2021 Issue Brief The Special Supplemental Nutrition Program for Women, Infants, and Children: Enrollment Before and During the COVID-19 Crisis, and February 10, 2022 Issue Brief Public Benefit Navigators Can Help Granite Staters Access Federal Assistance and Support the Economy.