New Hampshire’s State revenues, during both last fiscal year and thus far this year, have surpassed expectations and generated significant surpluses. These revenues, which appear to be fueled in large part by higher profits among national and multi-national corporations, add to the State’s strong fiscal position. This strength also includes flexible federal funds that the State can use to support an equitable and inclusive recovery from the COVID-19 crisis. Together, these resources and the ongoing higher revenues add to the substantial opportunity policymakers have to invest in services and a more vibrant and inclusive economy for Granite Staters.

State Revenues Higher Than Planned

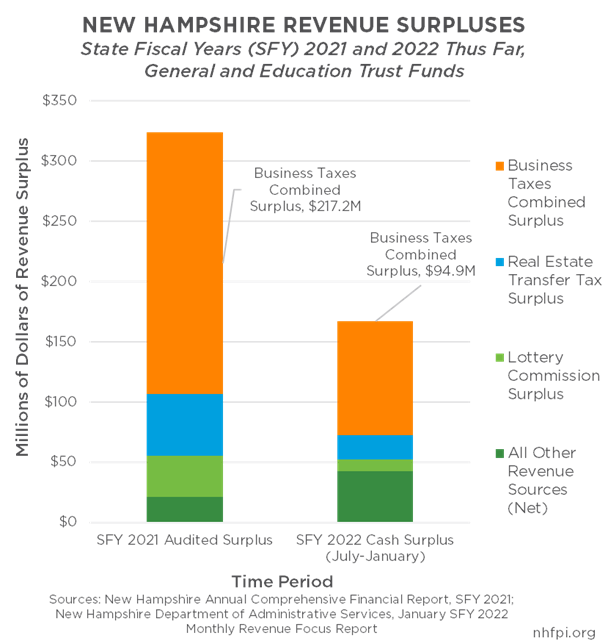

State revenues were substantially higher than anticipated in State Fiscal Year (SFY) 2021, which lasted from July 1, 2020 to June 30, 2021. The State’s Annual Comprehensive Financial Report, the final audit of New Hampshire’s finances in SFY 2021, recorded a revenue surplus for the General and Education Trust Funds of $323.7 million, or about 12.2 percent higher than the State Revenue Plan for the year established by the prior State Budget, crafted in 2019 and before the pandemic.

In addition, as of the end of January 2022, cash basis revenues for the General and Education Trust Funds were $167.0 million (13.8 percent) above the State Revenue Plan established in the State Budget passed in June 2021.

While New Hampshire’s revenue upswing is considerable, it is not out of the ordinary. Overall, states have seen significant revenue growth since their low points near the end of SFY 2020, including relative to pre-pandemic revenues. New Hampshire’s percentage revenue increases are similar to those of other states, and there is risk that this high revenue growth does not persist as economic activity slows, or as the real value of revenues fall relative to inflation.

The primary driver of these surpluses was the combined revenue from the Business Profits Tax and the Business Enterprise Tax, which are typically collected and measured together and not disaggregated until final returns are filed. In SFY 2021, the combined business taxes were $217.2 million (27.6 percent) above the State Revenue Plan, while all the remaining General and Education Trust Funds revenue sources combined were a net of $106.5 million (5.7 percent) above plan. In SFY 2022, through the end of January, the combined business tax cash receipts were $94.9 million (20.4 percent) ahead of plan, while all other revenue sources combined had added $72.1 million to the surplus, or only 43.2 percent of the total surplus. Notably, Real Estate Transfer Tax revenues were also significantly above plan, contributing substantially to the surplus generated by all other non-business tax sources.

Business tax revenues have been buoyed by a sharp rise in national corporate profits following the worst period of the pandemic. By one key measure from the U.S. Bureau of Economic Analysis, U.S. corporate profits in the third quarter of calendar year 2021 were 19.7 percent higher than in the same quarter in 2020, 22.4 percent higher than the third quarter of 2019, and 25.7 percent higher than they were in the third quarter of 2018.

This substantial increase in corporate profits is reflected in receipts from New Hampshire’s Business Profits Tax, which collects the majority of revenue from businesses filing as multi-national entities. The past two increases in revenue from business taxes have arrived following a more rapid increase in economic activity in the wake of the Great Recession, beginning in about 2015, and after 2017 changes in federal tax law that triggered a repatriation of assets previously held by corporations overseas. The reliance of business tax revenues on a relatively small number of large multi-state and multi-national entities for revenue suggests these trends in tax receipts are not necessarily reflective of changes in the state’s economy or business activity. Other revenue sources, such as the Meals and Rentals Tax or the Real Estate Transfer Tax, may be more directly reflective of specific sectors on New Hampshire’s economy than business tax receipts paid by corporations operating in multiple jurisdictions.

Surpluses and New Services Before the Next Budget

With State finances strong relative to revenue projections, the last State Budget ended on June 30, 2021 with a significant amount of unappropriated resources. The final State audit for the end of SFY 2021 also revealed State agencies underspent their General and Education Trust Funds budget appropriations by $222.1 million, a historically significant amount likely generated by pandemic-related disruptions to services. The two funds did carry forward a $54.4 million deficit from SFY 2020, but the underspending and higher revenues from SFY 2021 more than offset that amount. As with revenue surpluses, New Hampshire was not unique among states in having lower-than-anticipated spending levels.

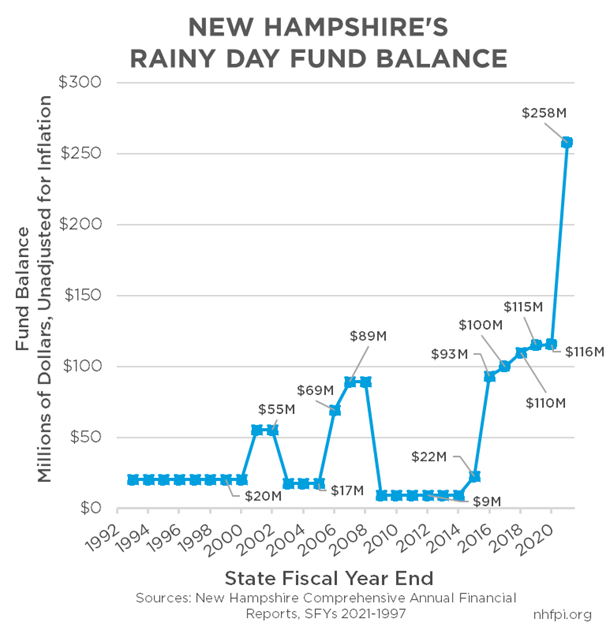

However, most of these surplus resources were shuttled to the State’s Revenue Stabilization Reserve Account, also known as the Rainy Day Fund. Language included in the current State Budget raised the cap on the Rainy Day Fund, allowing an additional $142.3 million in General Fund surplus dollars to get stored in the Rainy Day Fund, primarily for the purposes of offsetting future revenue deficits. As a result, the Rainy Day Fund balance was a historically high $257.8 million on July 1, 2021.

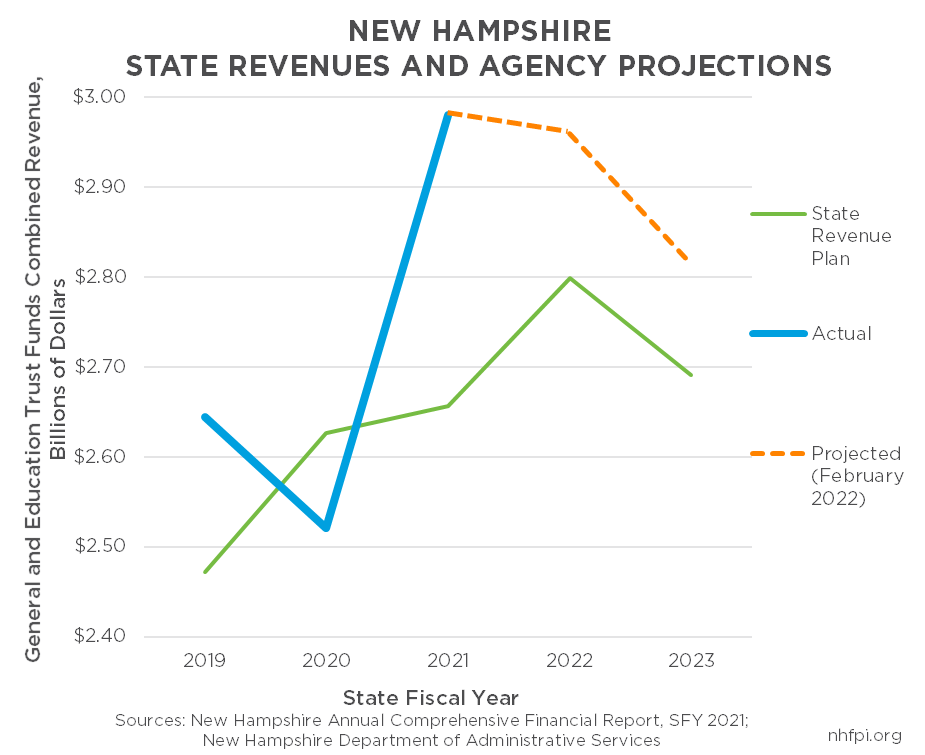

Although the General Fund surplus from SFY 2021 is less likely to be deployed for services during the budget biennium, current SFY 2022 revenues and newly-released revenue projections from the New Hampshire Department of Administrative Services suggest that there will be an ongoing budget surplus. However, they also suggest higher revenues will not persist, likely because of slower economic growth and ongoing tax reductions established by the current State Budget.

The State’s current revenue surplus in the General and Education Trust Funds of $167.0 million is significant, but any revenue deficits throughout the budget biennium could diminish or eliminate the surplus, depending on their magnitude. In other words, the surplus is not banked cash, and future revenues would need to be at least as strong as receipts anticipated by the State Revenue Plan to maintain the surplus.

State agencies are projecting an ongoing surplus for the next year and a half, but are not projecting revenues will remain as high as they were for SFY 2021. The projections expect revenues to be $160.8 million (5.7 percent) higher than plan in SFY 2022, and fall to $123.0 million (4.6 percent) above plan in SFY 2023. In total, the projections anticipate revenues will be $283.8 million (5.2 percent) above plan during the biennium.

Receipts from the two primary business taxes are projected to peak in SFY 2022, but then decline in SFY 2023, when the full effects of the reduction in business tax rates starting in Calendar Year 2022 for most businesses begin. Revenues from the Meals and Rentals Tax, which saw a reduction in its tax rate during SFY 2022, are projected to decline between SFY 2022 and SFY 2023 as well, while remaining well above plan for both years. Revenues from the Meals and Rentals Tax are also diverted from the General Fund to a dedicated fund to support aid to municipalities starting in SFY 2022. The Statewide Education Property Tax will contribute less revenue due to a one-year, temporary tax reduction of $100 million in SFY 2023. Projections for SFY 2023 also show a decline in Interest and Dividends Tax revenues from SFY 2022, likely reflecting reductions in the tax rate. Under current law, the Interest and Dividends Tax will slowly be eliminated, and estimates indicate nearly nine of out every ten dollars of benefit from the eventual elimination of this tax would flow to the top 20 percent of income earners, and almost half of benefits would go to the top one percent.

Flexible Federal Resources

While slowing economic growth and tax rate reductions could lead to a smaller State revenue surplus and fewer resources for services, the federal government has provided significant resources to support an equitable and inclusive recovery through the American Rescue Plan Act (ARPA). ARPA provided New Hampshire with nearly $995 million in relatively flexible federal funds, alongside additional funds for dedicated purposes and programs. These flexible funds, the Coronavirus State Fiscal Recovery Funds, are designed to provide resources to fight the pandemic, support families and businesses struggling with the health and economic impacts of the COVID-19 crisis, and, according to the U.S. Treasury Department, “build a strong, resilient, and equitable recovery by making investments that support long-term growth and opportunity.” These funds have additional permissible uses for aiding disproportionately impacted households and communities, including those with low incomes, in certain under-resourced Census tracts, and households receiving services from Native American Tribal governments. The U.S. Treasury Department identified that these resources could help address “the systemic public health and economic challenges that may have contributed to more severe impacts of the pandemic among low-income communities and people of color.”

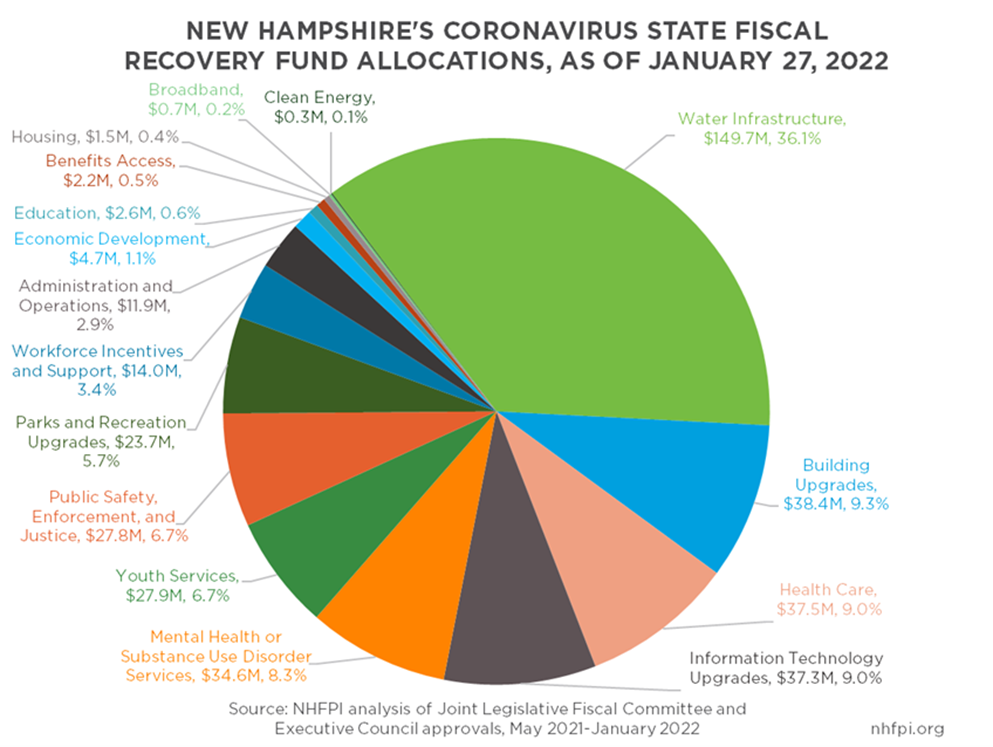

As of January 27, 2022, State policymakers, acting through the Joint Legislative Fiscal Committee, the Executive Council, and the Governor, have approved uses for $414.8 million (41.7 percent) of these funds. The remaining $579.7 million (58.3 percent) are unallocated, and must be allocated by or before December 2024, and spent by the end of 2026 or returned to the federal government.

State policymakers, based on recommendations from Executive Branch agencies, have appropriated more than half of committed funds thus far to water infrastructure projects, building upgrades, information technology improvements, and parks and recreation facility upgrades. Significant funds have also been allocated to mental health services, substance use disorder assistance, services for children and youth, and COVID-19 related health care expenses, such as vaccines and testing.

Future Considerations

The resources available to the State present a tremendous opportunity to aid the recovery from the COVID-19 crisis. Investments could help bolster the Granite State’s families and workforce, including the health care workforce, at a critical juncture for both the short-term concerns associated with the pandemic and the long-term demographic considerations for New Hampshire. Workforce supports could come in key areas of need, such as housing, child care and caregiving, and enhanced educational opportunities for both children and adults.

Flexible federal funds present a historic opportunity to make certain investments in these areas and help build a more inclusive recovery. Surplus General Fund revenues are even more flexible, as they can be deployed by policymakers largely without restriction, while the federal funds come with certain limitations. Tax reductions enacted in the current State Budget are projected to lead to revenue reductions during this budget cycle and in the future, limiting the opportunity to use these funds for key investments.

Assistance to Granite Staters, particularly individuals and families with low and moderate incomes, provides among the most effective forms of economic stimulus. With significant State and federal resources available, New Hampshire has an opportunity to build a stronger, more equitable recovery to benefit all Granite Staters.

– Phil Sletten, Senior Policy Analyst